We’re often asked where we find good companies. What is usually meant by this is where, in the economy, do we find good companies. But there is another way to think about the question, which examines the ‘where’ not in terms of economic sectors, but rather the company’s lifecycle.

S is for Sigmoid

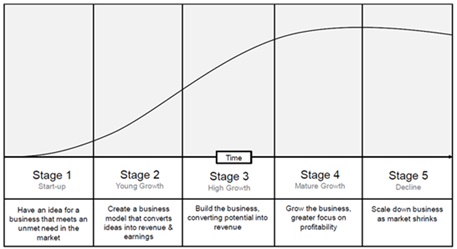

The starting point is to identify the different lifecycle stages and examine the attributes that businesses demonstrate at each stage. These stages are broken down on the following chart and overlaid with an s-curve (or sigmoid curve) to illustrate the growth and the level of risk in each stage.

Figure 1: The company lifecycle

Source: Seilern. For indicative purposes

At the earliest Start-up stage, the business is vulnerable. It may exist purely as an idea, scribbled on a napkin, or as a loss-making business that’s investing heavily in customer acquisition. Risk is high: 75 per cent of start-ups will not see their 15th birthday, and 90 per cent will not reach a mature stage of consistent profitability. Survival is exceptionally difficult. This is not a journey to take lightly or alone – almost all start-ups are financed by borrowing or giving away a stake in the business.

Investing in start-ups requires imagination and faith. It is best left to venture capitalists.

The next stage is Exponential Growth, where the goal is to grow quickly or, in the words of LinkedIn Founder Reed Hoffman, to ‘blitzscale’. These companies enjoy exponential growth and often see repeated and rapid doubling of their business. For them, the most important factor is the continuity of growth. Momentum and first-mover advantages are important; profitability is often a secondary concern.

This poses several problems. Firstly, it is hard to know what the future earnings profile of the business will look like. Secondly, it is impossible to value the business on a traditional profitability metric because there isn’t one, despite the inventive metrics conjured up by business analysts.

Investing in exponential growth businesses is like picking your racehorse for speed, before you’ve seen it jump a fence. Execution risks are high, and the breadth of outcomes (both upside and downside) is wide. It is a high-risk, high-return strategy.

Once the business has run the gauntlet of young growth, established a viable network and achieved the first benefits of scale, it reaches the High Growth phase. Here, sales are increasing, but the rate has declined from the dizzying prior stage. The company has proved its business model and cracked the formula for profitable growth. The strategic direction now shifts from pure growth to scaling the enterprise.

Most of our investments fall into this category and for good reason – growth is high and has proven sustainable. These businesses are the very definition of Quality Growth investing.

In the next Mature Growth stage, growth moderates, as the business settles into its strong competitive position, and margins expand. Towards the end of this stage, as the market becomes saturated or old, growth slows and the focus shifts from the top line to profits, often with disastrous consequences.

For companies here, a large improvement in profitability is not a welcome development but a sign that the business is squeezing the last drops from a slowing market. For the quality growth investor, it’s a signal that the business is approaching ex-growth and risks a material re-rating.

The last stage is Managed Decline. For these companies, sales growth has disappeared or gone negative. Their excellent profitability has attracted fierce competition, while business inertia has led to abandonment by capital markets, driving the stock price lower. This is the point in the lifecycle when many value investors invest, searching for businesses where they believe that the market has been unfairly harsh. This is a high-risk strategy. While value may be visible, the investor needs a catalyst to unlock that value.

R is for Risk

The reason the quality growth investor spends much time in the high-growth and mature-growth stages of a business is to manage risk. In a company’s early stages, there are significant uncertainties surrounding its viability or ability to generate consistent profitable growth. At the other end of the lifecycle, questions around the viability of the business arise again as it grapples with decline.

The quality growth investor is instead looking for businesses that can demonstrate growth in a sustainable and predictable way, and where the distribution of outcomes is narrowed to reflect the lower upside potential and lower downside risk.

MJ Faherty,

26th February 2021

1Of course, there is a great degree of overlap between the different stages and some stages last for much longer than others but as a generalised tool, the S-curve is very useful.

2Where the proportional increase in quantity is constant over time.

La presente es una comunicación de marketing / promoción financiera destinada únicamente a fines informativos y no constituye un asesoramiento de inversión. Cualquier previsión, opinión, meta, estrategia, previsión, estimación o expectativa, u otro comentario no histórico contenido o expresado en el presente documento está basado exclusivamente en previsiones, opiniones o estimaciones y expectativas actuales, y se considera, por tanto, una «proyección futura». Las proyecciones futuras están sujetas a riesgos e incertidumbres que podrían hacer que los auténticos resultados futuros difieran de nuestras expectativas.

Esta no es una recomendación, oferta o solicitud para comprar o vender ningún producto financiero. El contenido no está destinado a proporcionar asesoramiento contable, jurídico o fiscal y no debe ser utilizado para tales fines. Se cree que el contenido, incluidas las fuentes de datos externas, es fiable, pero no se ofrecen garantías al respecto. No se aceptará responsabilidad alguna en relación con la modificación, la corrección ni la actualización de la información aquí contenidas.

Tenga en cuenta que la rentabilidad histórica no debe considerarse una indicación de los resultados futuros. El valor de cualquier inversión y/o instrumento financiero incluido en este sitio web, así como las rentas obtenidas con ellos, podrían fluctuar y el inversor podría no recuperar el importe invertido originalmente. Los movimientos de divisas también pueden hacer que el valor de las inversiones suba o baje.

Este contenido no está destinado a ser utilizado por Personas Estadounidenses. Puede ser utilizado por sucursales o agencias de bancos o compañías de seguros constituidas o reguladas con arreglo a la legislación federal o estatal de Estados Unidos, que actúen en nombre o distribuyan a Personas No Estadounidenses. Este material no debe distribuirse a clientes de dichas sucursales o agencias ni al público en general.

Reciba información sobre nuestras novedades y eventos en su buzón de correo

"*" señala los campos obligatorios