In recent years, we have witnessed a rapidly evolving macroeconomic and geopolitical landscape, characterised by extreme volatility. This period has been marked by prolonged low and negative interest rates, an influx of unparalleled liquidity, and the worst pandemic in modern history, which triggered significant supply and demand shocks, leading to soaring inflation. Additionally, two international conflicts have reshaped the geopolitical environment, exacerbating the adverse effects of these events.

Central banks have assumed a pivotal role in navigating these turbulent waters, with significant shifts driven by changes in interest rates and interest rate expectations, alongside the deployment of unconventional monetary policies such as quantitative easing. Consequently, market timing has become even more challenging than usual. This dynamic was clearly illustrated in the US over the fourth quarter of 2023 and the first quarter of 2024, where market consensus swung from a deflationary bust to a disinflationary boom as the economy demonstrated unexpected resilience, and the Federal Reserve pivoted in December. Through the first quarter the market consensus shifted again to one of an inflationary boom and economic resilience, reigniting certain sectors of the economy. As a result, the Federal Reserve adopted a more cautious stance, making it unlikely that they will make the number of interest rate cuts expected at the beginning of the year.

Against this backdrop we have seen a rally in certain cyclical sectors. In such an environment, our funds have underperformed, primarily because we do not invest in the more cyclical sectors of the economy. As we have consistently emphasised, companies in these sectors do not meet our 10 Golden Rules. For instance, we refrain from investing in energy companies because their growth largely depends on the fluctuations of the economic cycle, they have no control over the prices at which they sell their goods, and they generally maintain opaque financial accounts. We also avoid most companies that operate in the semiconductor industry, which similarly exhibit highly cyclical growth patterns and offend our sixth Golden Rule that is designed to protect against customer and geographic concentration. Many of the companies in this space have one or more very large customers while at the same time are highly linked one way or another to Taiwan. While it is true that companies operating in these industries may generate stellar returns during upcycles, they are equally susceptible to significant declines when the tide turns. Furthermore, their earnings may be significantly impaired if they were to lose one of their large customers or were conflict to fall over Taiwan. Consequently, they fail to meet our stringent quality standards, which are designed to ensure long-term returns while minimising risk.

As Quality Growth investors, our primary objective is not merely to achieve returns but to do so while at the same time minimising risk. This is precisely why we avoid companies in these sectors, as we believe they carry a higher risk of deviating from the long-term returns we expect Quality Growth businesses to deliver over time.

Beyond the funds performing as expected in this kind of environment, what are the implications of an inflationary boom for equity investors if this is the environment we now find ourselves in? Is this scenario likely to be long-lived? If so, what will the implications be for interest rates? In such a scenario, investors should consider owning stocks that are insulated from the harmful effects of inflation and the structurally higher interest rate environment that accompanies higher inflation. Additionally, if the economy continues to perform well, when will the Fed start considering raising interest rates again? In that scenario, investors should also consider owning stocks that will not be harmed if this leads to a disinflationary boom or deflationary bust.

Disentangling this complex market environment is a challenging task. Although numerous forces influence stock prices—ranging from company fundamentals to industry dynamics, macroeconomic conditions such as interest rates and liquidity, market structure, and human psychology—we focus on a select few. None of these factors offer a definitive answer, which is why even the most accomplished investors can be wrong for extended periods. However, we believe that certain forces can be understood and analysed with greater confidence than others. For us, fundamentals (and to a lesser extent, industry dynamics) can be assessed with a reasonable degree of certainty, especially when it comes to Quality Growth businesses.

The fundamentals of Quality Growth businesses are more insulated from external market forces and are the most critical factor driving share prices, especially in the long term. In the current environment, Quality Growth businesses can offset the corrosive effect of inflation on cash flows (Inflation Series: Pricing Power, Inflation Series: Margins and Operating Leverage, Wimbledon and Inflation: You Cannot Be Serious!) and will be less affected by prolonged periods of higher interest rates because they do not rely on external capital in the form of debt or equity (The Debt Lag). Instead, they finance themselves through their strong and resilient cash generation. This absence of financing risk and the resilience of earnings power form the cornerstone of producing true, long-term returns.

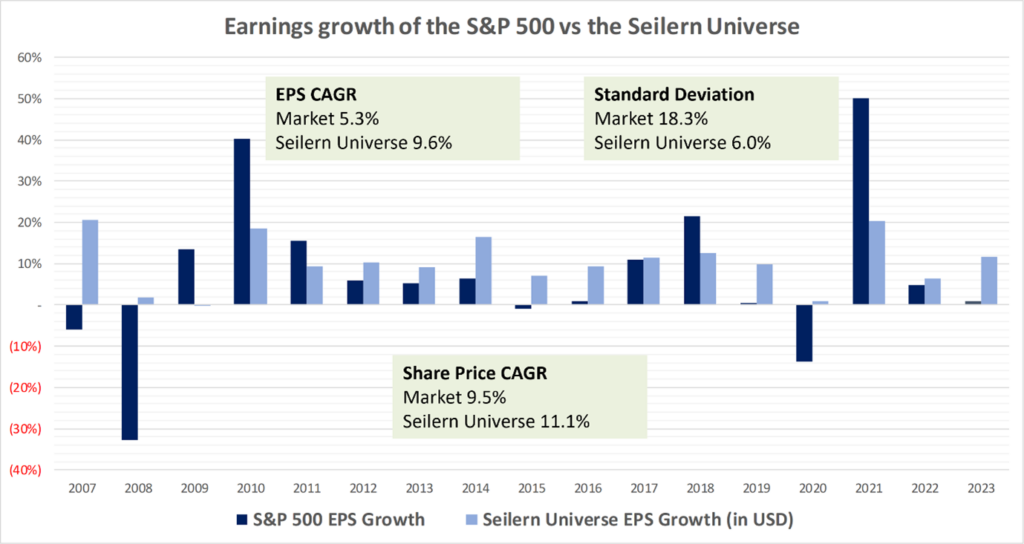

The predictability and stability of earnings are also paramount, as they have a significant impact on long-term performance. This is well illustrated by the graph below, which charts the earnings per share (EPS) of companies in the Seilern Universe versus those in the S&P 500 since 2007. Over this period, it becomes evident that while the S&P 500 may exhibit superior growth during strong upcycles, the stability of earnings in the Seilern Universe drives superior earnings growth over time. This is particularly visible during complex environments such as 2008, 2009, and 2020. Remarkably, over the period from 2007 to 2023, companies in the Seilern Universe delivered EPS growth 81 per cent greater than the S&P 500 with only one-third of the volatility, as measured by the standard deviation of earnings. This stability and resilient earnings growth have subsequently been mirrored by similar price increases in the companies in the Seilern Universe.

Figure 1: Earnings growth of the S&P 500 vs. the Seilern Universe

Amid this multivariate macroeconomic debate, one thing remains clear: there is a high level of uncertainty, making precise asset allocation decisions increasingly difficult. As always, our recommendation remains consistent and straightforward: trust in the virtues of Quality Growth businesses—their ability to offset the corrosive power of inflation, weather recessionary environments, and remain resilient in high interest rate environments. Quality Growth businesses provide a robust foundation for long-term investment success, even in the face of macroeconomic and geopolitical extremes.

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields