As our investors will know well, the Ten Golden Rules are the guiding principles which we use to help us identify Quality Growth companies. One of these rules is having a solid financial position and the principle is easy to understand. We look for companies that have a strong balance sheet, with little or no debt. This is because leverage can make businesses less able to withstand sudden shocks (which can be hard to predict) and taking on more debt can be a sign that a company is facing diminishing growth prospects.

With the US federal funds rate the highest it has been in 22 years, financial markets continue to be split on whether we have reached peak rates, but the debate is increasingly shifting from how high interest rates need to go, to how long they will stay elevated. Macroeconomic indicators seem to be supporting both sides of the argument with some suggesting a looming recession is inevitable while others suggest the employment market and consumer spending are not slowing down.

As bottom-up investors, we generally stay away from trying to predict the unpredictable, but we also recognise that the risk of rates staying higher for longer has increased over the last few months. For that reason, we thought now might be a good time to discuss the impact of higher borrowing costs on the fundamentals of public companies.

The secular decline in interest rates since the 1980s has greatly reduced the importance of the cost of debt on corporate finances to the point that it can often be ignored. According to a study by researchers at the Federal Reserve Bank of Boston, the corporate interest expense ratio (interest expenses as a share of total debt) has come down from around 7 per cent in 1996 to only 3 per cent in 2022.1

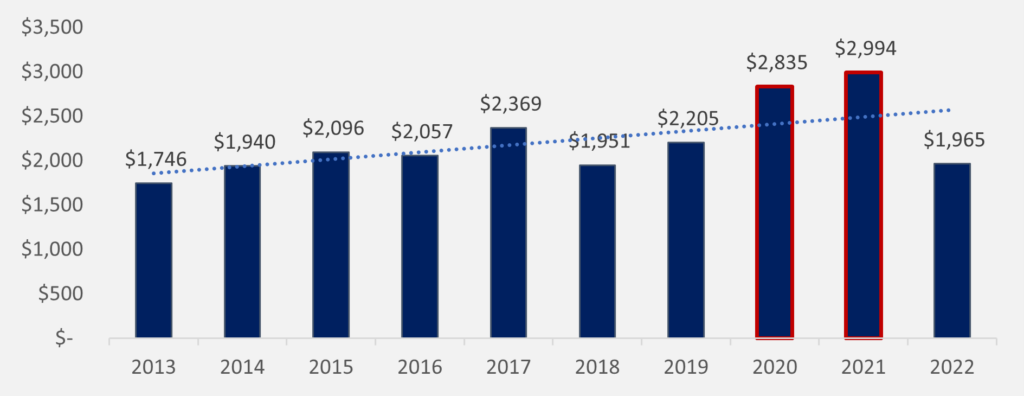

Interestingly, this expense ratio did not start to rise until the middle of 2023, almost 18 months after the first interest rate increase from the Federal Reserve. This lag effect can be explained by the fact that, during the pandemic, most companies used the record low yields as an opportunity to refinance their debt early and lock in attractive rates for the years to come. This is noticeable in the large increase in debt issuance that took place in 2020 and 2021, with US corporates issuing $3 trillion in debt on average each year compared to an average of $2 trillion annually between 2013 and 2019.

Figure 1: US bond issuance ($bn), 2013-2022

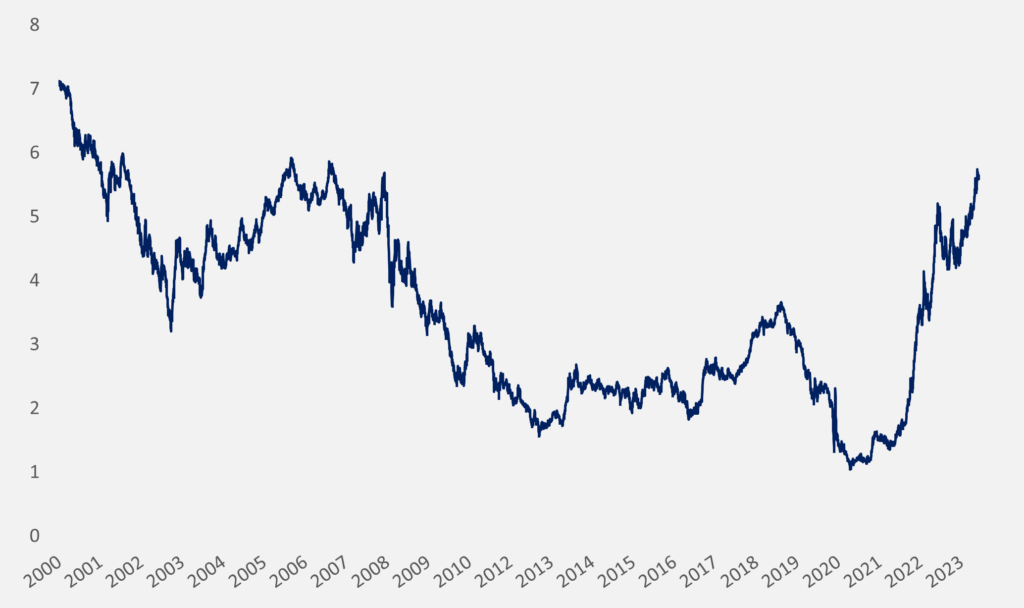

In hindsight, this was a great opportunity for companies to lock historically low interest rates just as the Federal Reserve was about to embark on one of its biggest tightening cycles. Since then, funding costs have increased by almost 4 percentage points with yields on investment grade bonds now at 5.6 per cent, a rate not seen since the height of the Global Financial Crisis and the dot-com bubble.

Figure 2: Yields of investment grade bonds (%), 2000-2023

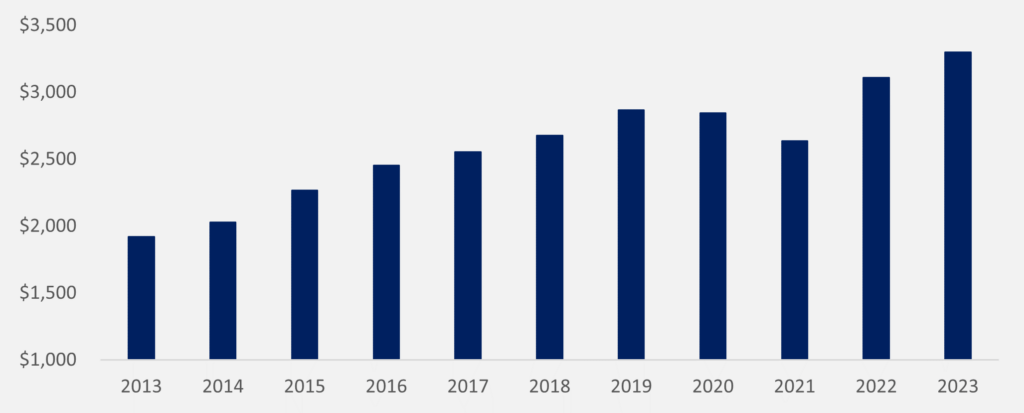

Despite the sharp rise in yields, companies have so far been able to delay the impact of higher interest expenses on their finances by delaying the refinancing of their debt in the hope that interest rates would normalise at a lower level. This delay has been particularly visible within the credit ratings sector with Moody’s reporting a decline in issuance volume of -40 per cent in 2022 compared to 2021. But the longer companies delay the rolling over of their debt, the larger the outstanding volume of debt that will need to be refinanced in the short term and the larger the impact from higher borrowing costs. The chart below shows how the volume of debt from US companies maturing in the next three years has sharply increased since 2021.

Figure 3: Outstanding debt maturing over the next three years ($bn)

Higher interest rates have therefore only just begun to impact the finances of companies around the world, and it is likely to accelerate over the next couple of years as companies refinance an increasingly larger share of their outstanding debt at current rates. With interest expenses representing on average 12 per cent of S&P 500 companies’ operating profits,2 most businesses should be able to weather higher interest expenses. But in the months and years to come, rising borrowing costs will begin to affect the earnings growth of companies and they will be forced to make some difficult choices. Some will prefer to reduce their leverage in order to protect their earnings, potentially curtailing their ability to reinvest in their business. Others will prefer to refinance their debt and accept lower net profit margins which will vary depending on the level of interest rates.

Neither of those outcomes seem attractive.

Fortunately, this is not a problem that the companies we invest in should have to deal with. This is because one of our key Golden Rules is that Quality Growth businesses should have a strong balance sheet with little or no debt. This is the only rule for which we have a hard quantitative limit, and we will sell any company that breaches this limit. This is best shown by the ratio of net debt to EBITDA of the funds, which currently ranges between negative 0.2x for Seilern World Growth and positive 0.3x for Seilern Europa. In other words, the average Quality Growth company within the funds has no leverage and will not see cash flows impacted by higher rates. Quality Growth investors will therefore be protected from higher borrowing costs should interest rates stay higher for longer.

1https://www.bostonfed.org/publications/current-policy-perspectives/2023/interest-expenses-coverage-ratio-and-firm-distress.aspx

2Source: FactSet, Seilern Investment Management Ltd.

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields