Monopolies are often seen as a clear sign of competitive advantage. The common belief being that high barriers to entry deter competition and allow the incumbent firm to prosper. However, having a monopolistic position does not always guarantee an enduring competitive advantage. On the contrary, history is littered with examples of once-mighty monopolistic companies being disrupted by new innovations which completely upend the status quo.

In this newsletter, we explore why having a monopolistic position can confer short-term advantages, but unless the incumbent can innovate and protect its competitive advantage, its monopoly status is meaningless in the long term. At Seilern, our research process is focused on finding companies that possess deep advantages and importantly, possess the ability to hold on to these advantages. In this way we can be sure companies have a sustainable, long-term competitive edge over peers. Our process is also centred around continually assessing the companies in our investible Universe against our 10 Golden Rules, and whether their advantages endure. As a result, if any companies possess monopolistic characteristics in the Seilern Universe, these are an output of our process rather than a pre-defined input.

Kodak’s moment

Why does having a monopoly confer advantages? The theory is that the incumbent that holds monopoly power is able to extract the maximum economic value from the industry in which it operates. In doing so, it is able to maximise its profits and pass these onto its shareholders. The issue is that being able to do this ad infinitum is challenging and fraught with tough decisions; should a company use today’s profits to fund investment efforts to expand its core markets, where short-term payoffs are most attractive, or should it try to fund longer-term projects in adjacent fields or disruptive technologies where the potential future payoffs are larger, but where uncertainty is greater? This dilemma can be compounded by inadequate remuneration policies which reward short-term performance at the expense of long-term growth prospects. Disruptive innovations therefore command less capital and managerial attention.

One of the most notable examples of this phenomenon is The Eastman Kodak Company,otherwise known as Kodak. The company was the first to pioneer mass-market cameras in the late-1800s and went on to develop a business model which included the entire value chain from cameras and film to photo development and printing. If you wanted to photograph a special event, it was likely you would be using a Kodak camera. The film from that camera would then likely be processed by Kodak and the prints would be made with Kodak chemistry on Kodak paper. Kodak was so successful in doing this that by 1976, the company had a virtual monopoly on the US film market with an estimated 90 per cent market share.1

In the 1990s, however, the shift from chemical film to digital electronics was creating demand for new types of products outside of Kodak’s core specialism. Not only was this new technology more convenient, it was also cheaper for the consumer. Instead of having to send off entire film reels and wait for them to be developed into photos, customers could now review their shots on the camera instantaneously and decide whether to save their photos or print them. This was a double whammy to Kodak’s profitable business model; customers would no longer need film in the first place and secondly the need to print photos would also be reduced with many preferring to keep images stored digitally. Competitors such as Sony, Nikon and Canon capitalised on this opportunity and gained a clear lead on Kodak in the digital camera market. In 2012, the company filed for bankruptcy.

A common misconception is that Kodak failed to innovate in light of this new, disruptive technology. In fact, Kodak was the first company to develop a digital camera in 1975 and patent its design in 1978.2 Despite this, the camera wasn’t put into production and was shelved. The company’s culture had a pivotal part to play in that decision. Management’s failure to fully grasp the digital opportunity was borne from the fact that Kodak’s business model had become so dependent on chemical film. The shift to embrace the digital side would have cannibalised its existing and highly-profitable film business. This internal resistance and inertia, in addition to strong competition on the digital side, saw the business model completely disrupted. Kodak had become a complacent monopolist.

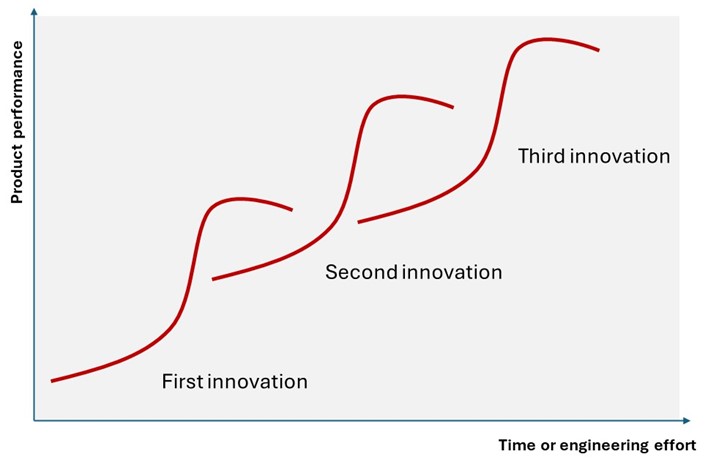

In his book, “Innovators Dilemma”, Christensen offers a conceptual framework that could be used to explain this phenomenon. He builds on the traditional S-curve (sigmoid curve) which identifies the different stages of a company’s or an innovation’s lifecycle. When a new technology is first developed, progress is slow, and the slope of the S-curve is more gradual, but then steepens as understanding and adoption improves, before plateauing and eventually declining as progress slows. As seen in the figure below, Christensen extends this thinking: when a new sustaining technology or innovation emerges, the S-curves of the old and new technologies overlap with the new technology in the early acceleration stages while the old plateaus.

Figure 1: The ‘technology’ S-curve

The most successful companies are those that can manage the transition from the old to the new technology as the curves overlap. In Kodak’s case, the first innovation was chemical film and was replaced by digital cameras. Digital cameras, in turn, were then disrupted by the third innovation of the smartphone which included digital camera functionality as standard.

Microsoft’s resurgence

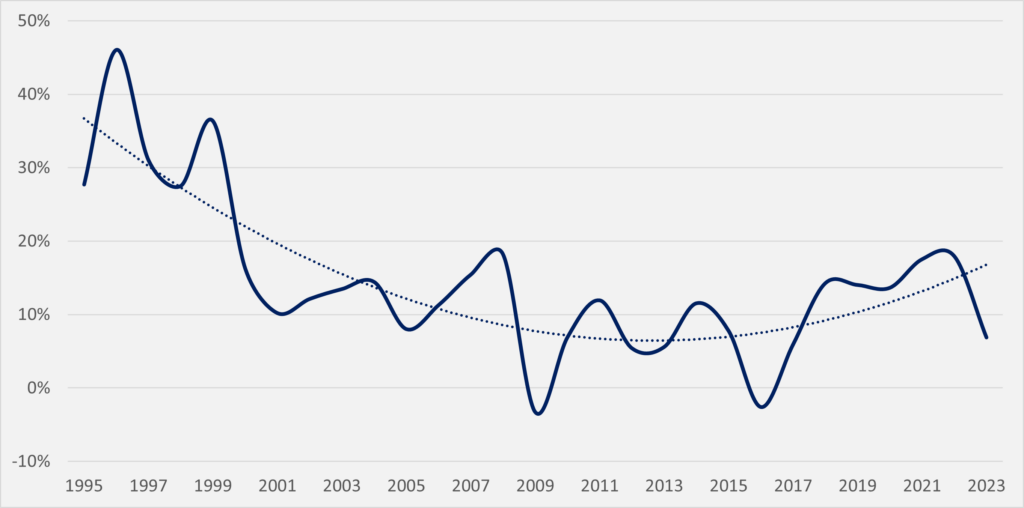

An interesting case study of such a successful transition is that of Microsoft. The company’s dominance of the personal computer market in the 2000s was unparalleled, with a 95 per cent global share of the operating system (OS) market in 2009, courtesy of its vastly successful Windows OS. Today, that figure is closer to 27 per cent.3 Looking at Microsoft’s sales growth in the figure below, the years 1995 to 2000 saw the company grow at an average of +30 per cent annually. This would fall to an average of just +10 per cent annually for the years 2001 to 2014. At this stage, one could have been forgiven for thinking that Microsoft was in the same camp as Kodak in letting a technological shift pass them by – the rapid rise of mobile operating systems (dominated by Android today).

Figure 2: Microsoft sales growth (% year-on-year), 1995-2023

However, the business today has been transformed dramatically from its OS-dependent days to having a highly successful Office suite, productivity software offering, gaming business, Azure cloud services and many other related services. Microsoft has been able to achieve a growth rate closer to +15 per cent on average since 2017.

A large factor in Microsoft’s success has been a shift in its mindset and strategy. By shifting investments in traditional technologies (e.g. operating systems) into new and emerging opportunities (e.g. cloud computing), the defensive, asset-protecting culture has changed to an offensive start-up-like-culture. A clear example since Satya Nadella became CEO in 2014, has been Microsoft’s transition into a device and platform agnostic company. Rather than relying on a closed-loop network, this has given Microsoft the ability to expand its technological tentacles, breathing new life into strategic partnerships and innovation. Had the company relied on its traditionally profitable operating systems business, akin to Kodak and its film business, it would be a very different entity today.

Capital allocation decisions aside, there are other factors which can also distract management teams from investing in long-term innovation. Perceived monopolies, given their market positioning, attract greater regulatory scrutiny to ensure consumers are being dealt a fair hand. Microsoft founder, Bill Gates, believes that had the company not been distracted by a US Department of Justice anti-trust investigation, which spanned 13 years (1998 – 2011), it would have had a credible mobile OS that rivalled Android.

We continue to see this today with ongoing anti-trust investigations against “Big Tech” companies such as Apple, Alphabet, Meta and Amazon, with regulators seemingly aiming for break-up orders. For a company in the crosshairs, this could eat up valuable resources and time, thereby de-railing any innovative projects that had or could have been undertaken. As we have written about in the past ((Anti) Trust in Politics), these investigations very rarely go to trial and even if they do, full-scale company break-ups are even more unlikely. Despite this, anti-trust action is one of the many risks we follow closely and manage carefully when constructing portfolios at Seilern.

Seilern’s process

While Microsoft has been very successful in managing multiple innovation shifts, the company goes one step further. Its relentless focus on its customer has given it a protective moat around its ecosystem, with many of its main applications ingraining themselves as mission-critical, non-core parts of its customer’ processes. So much so that even if ‘better’ alternatives to its products or services exist, the customer is tied into its growing ecosystem, resulting in extremely high switching costs. Only with a thorough understanding of these issues and the application of Seilern’s 10 Golden Rules can these conclusions be made regarding the durability of Microsoft’s competitive advantages and the likelihood of management’s strategy for growth succeeding.

In summary, monopolistic advantages are not guaranteed to endure in the long term. Rather than focusing on finding companies with monopolistic characteristics, it is much better to first understand the company and the industry in detail. At Seilern, our deep research process is geared toward finding companies that have, and can hold on to, a durable competitive advantage. In some cases, our process will result in us finding companies which have established some form of monopolistic or oligopolistic structure. What’s crucial here is to remember that this is purely an output of our research process, not an input.

1Kodak and The Digital Revolution – Harvard Business School (2005)

2https://patents.google.com/patent/US4131919

3https://gs.statcounter.com/os-market-share#monthly-200901-202402

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields