As the French proverb goes, the more things change, the more they stay the same. As we move into the second half of the year, with summer staycations on the horizon, gardens finally coming into full bloom and even the welcome return of Wimbledon fortnight here in the UK, change seems to be in the air. And yet at the same time, we have the all too familiar return of a British summer of wind and torrential rain, more delays to the full reopening of the economy and, for the readers of Seilern’s newsletter, a continuation of our series on inflation.

By now, you may have had your fill of questions of whether inflation is transitory, if it is in fact being driven by second-hand car prices, and the ‘will-they-won’t-they’ over whether the Fed will ever raise interest rates. For now, the US 10-year Treasury yield – which, at 1.5 per cent, continues to be as immovable as Novak Djokovic’s base line defence – is a good indication that things are staying the same. Nonetheless, inflation and the direction of interest rates will occupy the thoughts of market participants for some time.

By exploring how this potential changing environment could affect the cash flows, and therefore the valuations, of Quality Growth companies, we hope our series has provided a slightly different angle to much of the current discourse. This month we are going to turn to how inflation can lead to spiralling capital costs, thereby depressing cash flows, and why the ‘asset light’ nature of Quality Growth companies means that they are better insulated from insurgent inflation.

In earlier newsletters, Fernando and Marco discussed how pricing power and high margins can protect the operating cash flow of our companies. Other areas of the income statement can also be negatively affected by rising inflation. For example, taxes can rise indirectly because of lower depreciation, and indebted companies can face rising interest charges if higher interest rates accompany inflation. Fortunately, because Quality Growth companies have higher margins and lower debt than average, they are well positioned to bypass these pitfalls.

While net income is a key ingredient to strong free cash flow, we must not forget the other side of the equation: how a company’s operations are financed. Working capital requirements will dictate how much of this net income will drop through to operating cash. There are many moving parts to working capital which we will not be discussing in detail today, other than to say it is yet another complicating factor that must be considered when thinking about the overall impact of inflation on our companies.

Capital expenditure (CapEx) is another central element, determining how much operating cash flow is then left as free cash. Every growing company must invest some portion of its cash flows into building new assets, purchasing new machinery, or developing new software1 so that they can serve an increasing customer base. This is known as ‘growth’ capex. Every company must also spend a certain amount on maintaining its factories and replacing old machinery and software to serve its existing customer base. This is known as ‘maintenance’ capex. These capex plans are set out years in advance, and for those capital-intensive industries, financing arrangements will need to be in place at the start to fund any new expansion plans. The scope of these plans will depend on the capital intensity of the business and the growth aspirations of the company.

Budgeting for this spending is an important part of any corporate strategy. It could be disastrous if a company reaches the third year of building a plant, only to find out that their funds have run out and construction must be paused. A period of rampant inflation would make this budgeting process even harder.

A case study – the All England Lawn Tennis and Croquet Club

Since Wimbledon is finally upon us, I thought I would deviate from the usual corporate examples and discuss instead the recent capital expenditure of the All England Club (both the venue and the organiser of the Wimbledon Championships).

Due to its location in the damp north-west corner of Europe, Wimbledon has traditionally been beset with the issue of rain stopping play on its famous grass courts. Although this has in the past created some memorable scenes, including the somewhat bizarre one of Cliff Richard leading a singalong amidst a crowd of umbrellas, the sensible decision was made to construct retractable roofs on the centrepiece courts.

Centre Court was updated in 2009 and, in 2019, No.1 Court was completed. This latest refurbishment was no mean feat. At a headline cost of £75m, it involved the erection of eleven 65-ton trusses to hold up the mechanical roof, required a £175m loan and took four years to complete.

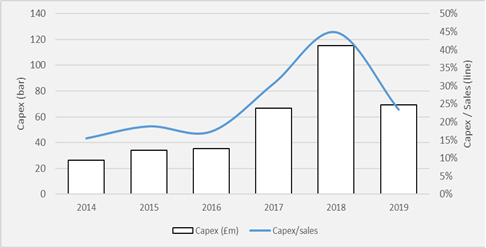

If we turn to the All England Club’s company accounts, we can see that its capital expenditure totalled £285m from 2016 to 2019. We can also see from previous years that it has a base spending level of circa £35m, which could be taken to be its annual maintenance capex2. On approximately £200m of sales, this gives the company a relatively high capex-to-sales ratio of 17 per cent. In the investment years of 2017–2019, this ratio rose to a peak of 43 per cent. Perhaps unexpectedly for an events business, if the All England Club was in the Seilern Universe, it would be by far the most capital-intensive!

Figure 1: All England Club Capex

The reasoning behind such large projects is clear. Increasing the guaranteed playing time each day, increasing the number of seats in the stadium, increasing the size and comfort of those seats and expanding corporate entertainment suites and facilities. All of these measures enable a greater volume of tickets and corporate packages to be sold, as well as providing justification for increasing prices each year. This higher level of spending fits firmly into the ‘growth’ capex bucket, and indeed the All England Club has enjoyed an impressive sales CAGR of 13 per cent over this period.

In reality, the project finished on time and on budget, a relatively rare phenomenon for a large-scale stadium construction project. Of course, it also happened in a period of stable and low inflation. But let’s just play out a hypothetical scenario and imagine that the project was launching now and that over the next four years, a period of higher inflation unfolds. How might things have been different?

The most obvious starting point is the price of materials. Those enormous trusses that allow the roof to move were part of the more than 2300 tons of steel which were delivered to the site in 2018 alone4. Since October, the price of iron ore has risen by 71.5 per cent, and the price of steel has risen even more. In this scenario, therefore, the project could already be seeing its raw materials bill almost double. On top of this, we have to think about shipping and the rising costs of all materials and parts imported from overseas. Container shipping prices have skyrocketed this year, with a container of cargo transported by sea from Shanghai to Rotterdam now costing a record $10,522 – 547 per cent higher than the seasonal average over the last five years5.

Finally, we need to take into account what would occur if significant wage inflation took place. Around 4,000 people worked on the project over the four years and a total of 2.2m man hours were completed. Labour costs would clearly have been a huge part of the overall budget. It currently feels strange to think of wage inflation being more than a couple of per cent, but we should remember that in the 1970s, UK wage inflation averaged 15 per cent6. Putting all of this together, we can imagine a scenario where this project takes place amidst 15–20 per cent inflation each year. Thus, from the year of the project being announced, such a project could end up running over by 50 per cent and perhaps even doubling.

For the All England Club, the near doubling of a £75m project would be painful, though probably not disastrous. Its operating cash flow has varied between £60–90m over the last few years, so the overspend would effectively set them back a year. Given the brand and the certainty of future cash flows, accessing another loan would probably not be too difficult. The same would not be true of most capital-intensive public companies. A new loan, if it could be accessed, would likely come at a higher rate, reducing profits further. If that company was already heavily indebted, this could lead to a breaching of debt covenants. It might even force the company into an equity raise. None of these outcomes would be taken well by investors.

It is interesting to note that except for its capital intensity, the All England Club shares many of the core characteristics of the companies in the Seilern Universe: strong growth and predictable revenues, high margins and a solid financial position. The key difference is that our companies would be further protected by being capital light. The average capex-to-sales ratio of the Seilern Universe is only 4.8 per cent. So, a doubling of capex would not come close to absorbing a full year of operating cash flow. Further, the high margins of our companies means that that even an increased level of capex can be swallowed by a strong level of operating cash. And since they carry little debt and are often net cash, even if this higher level of capex did lead to negative free cash flow, it could be funded without having to raise debt or equity. On this last point, we observe that companies with high capital intensity also tend to have higher levels of debt, which they require to finance these growth projects. This is another reason why we try to avoid capital-intensive businesses.

Despite the vast amount of column inches devoted to inflation over the past few months, the question is not going away any time soon. Over the course of this series, we have tried to present two core beliefs. First, the impact of inflation and rising interest rates on the valuation of companies is extremely complex and involves a multitude of different considerations. Second, Quality Growth companies have the characteristics that will allow them to prosper if such an environment does unfold. These include:

- Pricing power which enables them to combat rising costs;

- High margins and operating leverage, allowing them to scale into that pricing power; and

- Low capital intensity, so that they can continue to grow in an unconstrained manner.

These characteristics significantly reduce the risk of potentially catastrophic outcomes, which is far more important than whatever fall in valuation that comes from an increase in discount rates. This is particularly reassuring when you are dealing with something like inflation, which is more complicated than one of Nadal’s pre-serve routines and as contentious as a John McEnroe-disputed line call.

1Only certain types of software qualify for capitalisation, notably software that has been acquired or developed only for the internal needs of the business.

2The eagle eyed will have noticed that the £75m of headline cost of the No.1 project is far outweighed by the ‘growth’ capex in each year in excess of the £35m ‘maintenance’, by almost £100m. The All England Club will have various projects on the go simultaneously that do not necessarily receive the same publicity as a stadium expansion.

3Compound annual growth rate.

4Sir Robert McAlpine, https://www.srm.com/projects/refurbishing-wimbledon-s-no1-court-london/

5Drewry Shipping, Bloomberg

6Office for National Statistics, https://www.ons.gov.uk/economy/grossdomesticproductgdp/timeseries/kgq2/qna

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields