The concept of using diversification to reduce risk without sacrificing returns is one of the central tenets of Harry Markowitz’s seminal work on portfolio management theory1. After 67 years, it continues to be a fundamental building block of portfolio management, but it is often drawn upon to justify holding large portfolios of securities with so-called ‘low idiosyncratic risk’ that comes from buying the haystack rather than looking for the needle2. Today, many investor portfolios have become bloated with securities, where the actual intention is not to diversify risk but to spread capital across many securities to limit the downside impact of each single one. As well as being a recipe for mediocrity, this is a gross misunderstanding of what diversification ought to stand for in the context of portfolio construction.

Diversification and its limits

At its core, diversification is an important tool that is designed to distribute risk sensibly across a portfolio of securities. It helps to avoid the impact on a portfolio of a company-specific mishap. The major misconception of diversification is that spreading capital across a number of names is sufficient to claim that the portfolio is diversified. This is not necessarily true. Diversification ought to be thought of in the context of risk management and as such, it is diversification of the risks that pertain to the individual companies, and not the companies per se, that is important.

For example, diversifying capital evenly across the stock of 50 companies may seem like risk is spread across 50 companies. However, if ten of the 50 are involved in the production of oil and gas, this so-called ‘diversification’ may not offer adequate protection. Another investor that diversifies capital across ten different companies, but where the companies operate across different industries or have a breadth of risk exposures, may find a greater level of diversification than the investor with five times as many holdings.

Even in a portfolio with a diverse risk profile, there is a natural limit to the benefit of adding new securities. As each new, uncorrelated stock is added, the law of diminishing marginal utility takes hold and the incremental usefulness shrinks.

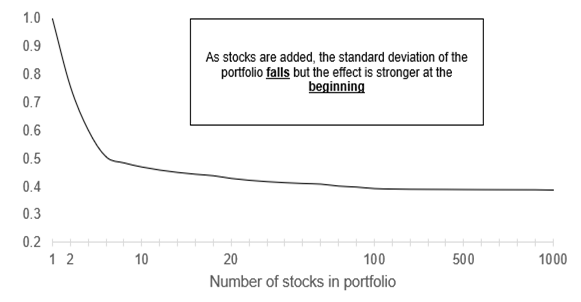

Figure 1: Portfolio Standard Deviation

This was illustrated by Statman2 (Figure 1), where he showed that the benefit of going from a one-stock to a two-stock portfolio decreases portfolio standard deviation by 25 per cent, while going from a 20-stock to a 30-stock portfolio decreases portfolio standard deviation by an incremental 3 per cent. Taking this to the extreme, adding 900 new and uncorrelated stocks4 to a 100-stock portfolio only decreases the portfolio standard deviation by another 1 per cent!

While we agree with the underlying mechanics, we take issue with the use of the standard deviation of stock prices as a measure of risk. Standard deviation is popular in large part due to its availability (all you need is a series of stock prices and a formula) but it is not the best measure of business risk5. This is because standard deviation is a measure of the past performance of a stock and reveals surprisingly little about the current health of a business or, perhaps more importantly, its future prospects.

The principle, however, is useful in providing a framework for the investor to understand the different risk exposures of companies and as a consequence, the portfolio as a whole. But knowing the risks is just the first step, the investor must then diversify these exposures. As long as there is proper thought given to the risks, with special effort made to avoid the bulking in any single one, this approach will allow the true mechanics of diversification to work.

Quantity versus Quality

There is also a question of whether adding more investments in lieu of quality, in-depth analysis is a prudent strategy. We think not, and agree with Philip Fisher6:

“Investors have been so oversold on diversification that fear of having too many eggs in one basket has caused them to put too little into companies they thoroughly know and far too much in others about which they know nothing at all. It never seems to occur to them, much less to their advisers, that buying a company without having sufficient knowledge of it may be even more dangerous than having inadequate diversification.”

Our strategy at Seilern is to build concentrated portfolios of approximately 17-25 securities that we feel comfortable holding through a challenging market. These are businesses whose stock prices may go down, but where the underlying businesses will not be permanently impaired and will not force the investor to realise a permanent loss of capital. A pre-requisite of this approach is that we must have a deep knowledge of the businesses. This means both an understanding of their returns and an understanding of their risks. It also means understanding the relationship that these risks have with one-another in the context of the portfolio. This approach is best suited to the concentrated portfolio. By reviewing fewer securities, each one can be analysed in greater depth. Knowing fewer things, but knowing them well, is a recipe for properly understanding the risks involved.

One comment we often receive at this point is why we cannot simply add more analysts in order to increase the number of well-researched companies in our portfolios? While this approach may work for some investment management houses, it is not always a practical solution. This is for two reasons. First, at Seilern, the decision-making authority for the fund rests with the fund manager. Each decision must be channelled through this individual, as they are best placed to take a holistic view of the risk profile of the fund. As such, the same ‘bottleneck’ continues to exist irrespective of the volume of research nodes that are added. Second, as research capacity is added, the efficiency with which information is communicated amongst the team degrades. As with other aspects of our business, we value quality over quantity.

Concentrated Portfolio, Diversified Risk

Both concentration and diversification, contrary to popular wisdom, are not opposing principles but complimentary ones, that together help to optimise risk management. Concentrated funds allow the construction of informationally-efficient and well-researched portfolios, while diversification seeks to identify and minimise what we see as real risk; not measures based on derived stock price statistics but the true underlying business risks of the companies.

1Markowitz, H. (1952), “Portfolio Selection”. The Journal of Finance, vol. 7, No. 1, pp. 77–91.

2“Don’t look for the needle in the haystack. Just buy the haystack!”. Jack Bogle. Founder of The Vanguard Group, the second largest provider of exchange-traded funds (ETF’s) in the world.

3Statman, M. (1987), “How Many Stocks Make a Diversified Portfolio?”. Journal of Financial and Quantitative Analysis, Vol. 22, No. 3, pp. 353-363 and Statman, M. (2004), “The Diversification Puzzle”. Financial Analysts Journal, Vol. 60, No. 4, pp. 44-53.

4In his 2004 study, Statman assumed the correlation between each of the securities to be 0.08.

5Neither is correlation, which uses standard deviation as an input and tends to understate the correlation between stocks in a bear market. Chua, D. & Kritzman, M. (2009), “The Myth of Diversification”. Journal of Portfolio Management, Vol. 36, No. 1.

6Fisher, P. (1958), “Common Stocks And Uncommon Profits”, Harper & Brothers.

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields