Approaching the halfway point of the year, and with markets seemingly leading us into an early summer lull with a recent bout of calm, it would be tempting to say that 2023 has been a very different year to 2022. However, while the trajectory of share prices has changed, we would argue that the macroeconomic picture remains as unclear as before. There is still huge uncertainty around inflation and interest rates; geopolitical tensions continue to rise; we are still navigating the banking crisis set off by the collapse of Silicon Valley Bank (SVB); and AI is apparently set to disrupt everything.

The last three years have been filled with so many ‘events’ that we are reminded of Lenin’s famous quotation, “There are decades where nothing happens; and there are weeks where decades happen”. It feels as if this period has been full of such weeks.

How to deal with volatility

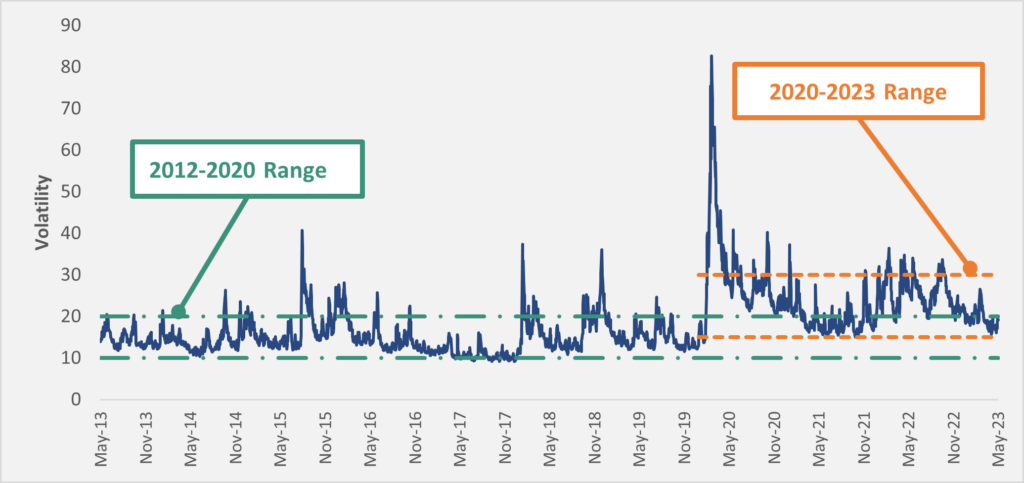

This feeling of elevated volatility is reflected in the data. If you look at a long-term chart of the VIX index (which measures market expectations of volatility) from 2012 the VIX mainly traded in a range of 10 to 20, with the occasional, brief spike above 30. Since 2020, the range has shifted to 15-30 with that 30 level being breached more than 10 times, often for multiple days. As a fund manager, when faced with periods of high market volatility you have, broadly speaking, two options. You can take a view on the macro and trade accordingly. Or you can adopt a strategy that means you don’t have to, which is the approach we take.

Figure 1: VIX Index, 26th May 2013- 26th May 2023

The problem with taking a view is that you may be wrong. Even if you somehow manage to predict correctly how macro conditions will evolve, you are still left with the perils of market timing. This is risky for multiple reasons, but most importantly, by market timing and trying to avoid the worst days, you risk being out of the market for the best ones (Market Timing). This is in fact quite likely given that these extreme performance days tend to occur in periods of high volatility. So being able to take advantage of those best days, while avoiding the worst is very difficult and certainly not something we believe we can do.

Managing risk

Of course, it is hard to completely ignore market volatility, but we do have a process which means we don’t refer to it when making our investment decisions. This is because, unlike many others, we don’t equate stock volatility to risk. As long-term investors, the real risk is that our companies fail to generate the earnings, or cash flows, that we forecast and we end up incurring a permanent loss of capital.1

The first way we manage this risk is by excluding a lot of ‘riskier’ industries from the beginning. As Marco outlined in our March newsletter (The Power of Exclusion), we exclude roughly 50-60 per cent of potential companies because of our Ten Golden Rules. These are the minimum set of criteria which all of our companies must meet before we can invest and there are quite a lot of entire industries that, by their own definition, do not meet these Rules. We therefore exclude them from the start.

For example, banks fall down on many of our golden rules but perhaps most importantly, they do not have clear and transparent accounts. This makes it hard to understand their balance sheets and to evaluate the level of risk we would be taking on by investing. We witnessed this during the GFC and only 15 years later, the collapse of SVB, First Republic and Credit Suisse have yet again demonstrated this fact.

The second way we manage risk is by knowing our companies intimately. We have a nine-person investment team, which carries out in-depth research to help us identify those companies that are less exposed to the ups and downs of economic cycles, and that have the defensive characteristics to protect them in tough times. The team is continually analysing and re-assessing our companies. This gives us the confidence to back our own investment theses, rather than obsessing over the vagaries of share prices. It is hard to convey briefly in a newsletter the lengths we go to when researching new ideas and covering our portfolio companies. Our base reports at least reflect a part of the process. These are initiation documents that we must write on companies before they can be added to the Universe. They vary in length from 80 pages to more than 200 and can take up to 12 months to write. Detailed analysis of the industry, the competitive positioning and the company’s long-term strategy, as well as its strengths, weaknesses and risks, is included. We look closely at the assumptions going into the financial models and the 10-year DCFs that are at the heart of our valuation. And there is a careful assessment of the corporate governance frameworks, incentive structures for management and the underlying ownership of the business. This all reflects hours of trawling through annual and quarterly reports, earnings transcripts and industry reports in addition to conversations with customers, former employees, competitors and the management themselves. And finally, it is subject to constant peer review and feedback at our regular (and frequently intense) investment meetings. In short, it is a lot of work!

The benefits of a long-term approach

The other factor that helps to prevent us being distracted by volatility in markets is our long-term approach. Long-term investing is a core belief at Seilern. Our culture and business are designed to support that philosophy, from our partnership structure and remuneration policy through to our distribution efforts and, above all, our investment process.

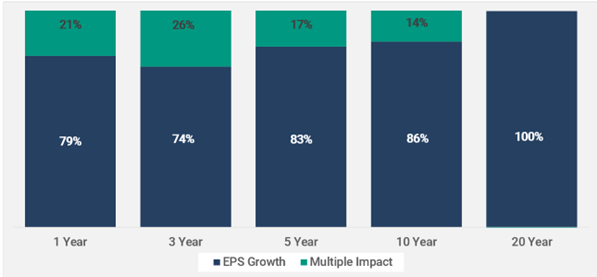

Many people think that long term means a year or even six months. We are genuinely long term. Our average holding period in our funds is six years, we have held many positions for more than 10 and some for more than 20. While we believe earnings drive share prices, their impact becomes ever more important the longer your holding period. Over short and medium time horizons, there is still quite a large contribution from multiple expansion or compression in the overall return of a share. But as you go out further the importance of the multiple becomes less. In our analysis of the returns of the S&P 500 over the past 60 years, over rolling 20 year periods all the returns can be attributed to the earnings growth of the company. Now that provides no comfort if you experience short-term underperformance, especially when it is as pronounced as last year. But the worst thing you can do is to then trade and thereby crystallise a loss. Ultimately, as long as a company can continue to generate sustainable earnings growth, we will continue to hold it.

Figure 2: S&P 500 Return Decomposition 1962-2022

Staying the course

Our investment team is always striving to verify that our companies still have the ingredients to enable this growth. Amidst all the volatility over the past 18 months, the fundamentals of our companies have remained resilient. This is reflected by the fact that this year they have seen, in aggregate, earnings upgrades, versus the overall market which has seen downgrades. In fact, most of our worst performers in 2022 have been the best performers this year. While some of this can be attributed to changes in interest rates, an important factor is that throughout this period, they have continued to show the sustainability of their long-term earnings growth, often alongside excellent interim results. This demonstrates that while volatility and external factors can have an impact on individual stocks for some time, eventually the fundamentals of the business will prevail.

At Seilern, we are far more interested in the fundamental performance of our companies’ earnings than the short-term direction of their share prices. Our primary focus is to deliver consistent and concentrated portfolios of Quality Growth companies for our clients and our aim is to continue doing this regardless of the levels of macroeconomic uncertainty or market volatility.

1This could theoretically play out in a variety of ways but a hypothetical example would be that we invest in a company that is lower quality than we initially assess, and posts revenue growth below expectations which leads to a couple of profit warnings. This prompts further research that shows the company does not enjoy a sustainable competitive advantage, and therefore has broken one of our Ten Golden Rules, which forces us to sell the position at a depressed value, before any further profit warnings materialise. This would thereby incur a permanent loss of capital.

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields