Discounts are curious things. Each year on the 26th of December, shoppers queue outside stores and flood websites to buy things that have fallen in price. The products haven’t aged, expired, or lost utility; only the price has changed, and this change is widely welcomed.

This behaviour, however, isn’t limited to post-Christmas sales. We love seasonal sales, back-to-school sales, cultural holiday sales and Independence Day sales. We love ‘Singles’ days, ‘Black’ Fridays and ‘Cyber’ Mondays. For some products, full price is almost a total fiction – when is the last time you bought shampoo or toothpaste without getting “50 per cent extra, free”? We are very much conditioned to look for and to like discounts. It is a normal part of the human psyche.

Yet this intuition breaks down in the stock market. When the price of a stock falls, it is rarely welcomed. Instead, it is treated as evidence that something has gone wrong, even when the real evidence, the performance of the underlying business, shows no signs of trouble. Moreover, the larger and more persistent the decline, the stronger that assumption becomes and the harder investors look for signs.

For our Quality Growth strategy, the last five years have been a period exemplified by this stock price/fundamentals disconnect. While the underlying earnings of our companies have continued to compound at a healthy rate, this has not been rewarded.

Many observers watch prices of stocks and funds closely and, after such a period, extrapolate the recent past into the future, selling out of ‘losing’ funds and stocks and piling into ‘winners’. However, some knowledge of valuation and of the durability of high-quality business fundamentals suggests the opposite: when prices lag the underlying earnings of resilient businesses for an extended period, the future return potential is not diminished but enhanced.

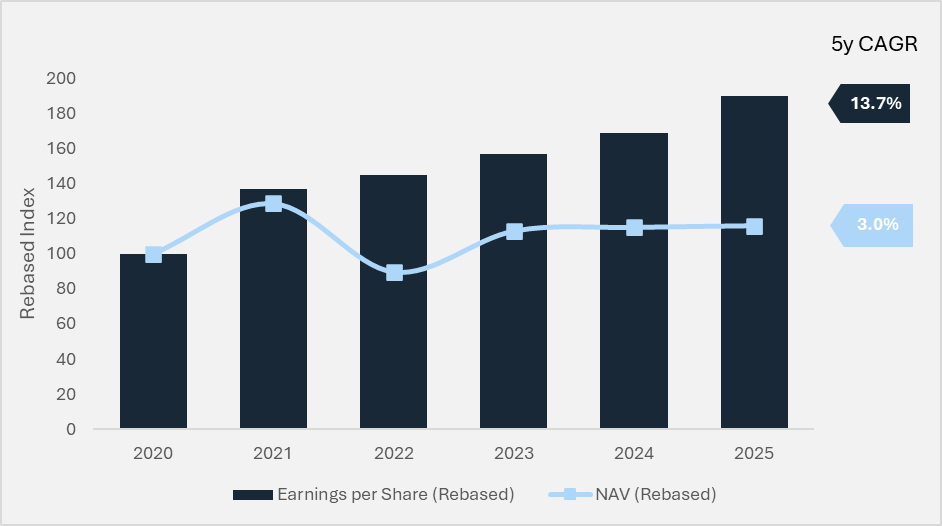

Breaking Down Returns – The Last Five Years

The fundamental premise of Quality Growth is that over the long term, a stock price will track the growth in a company’s earnings (Focusing on the Fundamentals). We have fielded many questions as to why the stock prices of our businesses have not trended toward their earnings over the last five years, arguably a long enough period for this dynamic to emerge. To understand why this disconnect can persist, it is helpful to break down the drivers of returns:

Price returns are a function of earnings growth and the changes in the price that the market is willing to pay for each unit of earnings (the price/earnings ratio). While earnings growth has been remarkably stable over a number of decades for the Seilern funds, the multiple that the market is willing to pay for each company’s earnings has not.

Sometimes the market places very low multiples on businesses for reasons that later prove to be overdone or temporary. It is normal in these periods for price performance to lag earnings growth and for investors to question the viability of the strategy. Sometimes the market does the opposite and places very high multiples on companies, equally without merit. It is normal in these periods for price performance to outpace earnings growth and for investors to question the viability of other strategies.

In the lead up to 2020, Quality Growth suffered the second problem. With low growth and low inflation in a post-global financial crisis world, companies that could grow their top and bottom lines sustainably were rare. Investors, hungry for returns, flocked to the asset class as interest rates were pinned to the floor. This inflated valuations and helped to drive returns over that period far beyond the level of underlying earnings growth. Put simply, the multiple expansion in the equation above was disproportionately driving returns. This had two knock-on effects. First, this high starting point meant that future returns were compressed because investors were paying more upfront for the same stream of future earnings; and second, elevated valuations made these companies more vulnerable to any development that caused investors to question whether those valuations were justified.

Of course, the subsequent five years provided these events in abundance, ranging from a global pandemic, the return of inflation and an interest-rate hiking cycle, to extreme capital flows out of ‘underperforming’ active managers and into ‘outperforming’ index funds, and most recently, to questions about the viability of business models with the advent of artificial intelligence (AI).

The degree of compression that these events exacted upon the prices of Quality Growth companies is remarkable. The 1-year forward P/E multiple of Seilern World Growth halved from 41.3x at the end of December 2020 falling to 21.7x at the end of March 2026.1

Equally remarkable is the resilience of Quality Growth companies’ earnings during this turbulent period. From December 2020 through December 2025, the earnings growth of Seilern World Growth has compounded at 13.7 per cent (versus an NAV that has compounded at 3.0 per cent).2

Figure 1: Seilern World Growth Earnings Per Share versus Seilern World Growth NAV

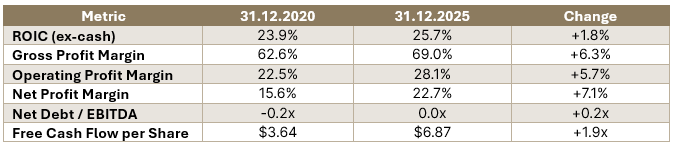

Is a halving of the price/earnings multiple warranted? Perhaps these companies are simply lower quality than they have been in the past? The numbers do not agree. Measures of quality, from ROIC to margins, have broadly been improving:

Table 1: Fund Metrics Comparison (Median)

With the advent of AI and its vast potential, the claim might be made that the value of these companies lies not in what they have achieved historically, but in what they can achieve in this new world. Yet, as we have discussed in previous newsletters, these companies have features which help to defend them against potential disruption and they may in fact end up being major beneficiaries of AI. This is a topic we will cover in more detail in our upcoming webcast, but our view is that it is unlikely that the earnings of most of our companies are going to be materially affected by AI in the short-to-medium term. And for those that may be affected, current valuations already reflect this fear and heightened level of uncertainty.

Where We Stand

Today, the starting point has materially improved versus five years ago. Earnings expectations have continued to be low double digit and are supported by higher quality businesses. Starting valuations are also significantly lower both relative to their own history and relative to the market average, providing, at worst, a platform for stability and, at best, a tailwind of multiple expansion.

Table 2: Price Return Matrix

Moving from external measures of valuation (P/E ratios) to our internal measures (Discounted Cash Flows), return expectations have seldom looked as attractive. Today, the annualised five year expected return, a measure based on our estimates of cash flow growth and valuation, for Seilern World Growth sits at 14.7 per cent, a level we have not seen since rate hikes led to the bottoming out of long-duration assets in 2022. The catalyst of that duration unwind has also lost some steam with long-term US inflation expectations remaining well anchored despite recent market turmoil.3

It is worth remembering that underperformance, painful as it is, can often be the price of admission for a non-consensus, high-conviction strategy. Investment styles don’t stop working because they are wrong; they stop working because styles, like the seasons, have cycles where they work and cycles where they do not.

If a stock price ultimately reflects the present value of future cash flows, and those cash flows continue to grow, patience becomes our greatest virtue as we wait for the cycle to turn. In this context, lower prices are not a signal to retreat but a reflection of improved prospective returns. And, when high-quality businesses are available at meaningful discounts, the situation is no different from the 26th of December. The only question is whether one has enough conviction to join the queue.

1Reaching its peak in December 2021 of 42.8x.

2Seilern World Growth USD UI share class as at 31 December 2025.

3The US five-year, five-year forward inflation rate, indicates market inflation expectations for the five-year period beginning in five years’ time. It is the price of long-dated inflation risk, a key input for long-term yields and has been remarkably stable, even falling since the beginning of the year to 31 March 2026.

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields