Earnings growth drives stock returns

The underlying principle of our investment philosophy is that, over time, earnings growth will drive share prices. With this in mind, we look for companies that are able to grow their earnings at as high a rate as possible, with the caveat that we want them to be able to do this in a sustainable way. We believe that this translation of earnings growth into share price performance is only afforded to the sensible long-term investor. Below we discuss why we believe this to be true.

Voting vs Weighing – The perils of the short term

A most useful illustration of the pitfalls of trying to invest in the short term1 is an analogy coined by Benjamin Graham, a pioneer in early security analysis, where he noted that in the short term, the stock market is analogous to a voting machine, tallying up the record of which firms are popular and unpopular, while in the long term, the stock market has more in common with a weighing machine, making a more thoughtful judgment as to the substance of a company. We have found this to be broadly true. The near-term popularity contest often ignores or misprices fundamental drivers of earnings power, with excessive pessimism compressing valuations and irrational exuberance bidding them up to eye-watering levels. In the meantime, the ‘true’ earnings power of the businesses may not have changed much. All of this means that in order to be successful in the short term, you not only have to get the fundamentals of the business correct but you must also get the temperature of the market right. This is no small feat.

The Business and The Stock

Digging a little deeper, we can break down the source of near-term uncertainty into two parts. The first is the uncertainly related to the expected earnings of a business and the second is uncertainty as to the appropriate price to pay for each unit of earnings2.

What we illustrate below is that usually it is not the uncertainty related to the earnings that causes the controversy. This is because companies often give broad levels of guidance, which is augmented by analysts’ own assumptions and data ranging from customer surveys to satellite imagery of factory car parks. Instead, it is the uncertainty around the appropriate multiple to pay for those earnings that proves contentious. As we will show below, there is a significant difference in the level of uncertainly of these two items.

If we take the world’s largest company, Apple Inc., as a proxy for coverage (under the theory that the greater number of estimates, the more likely that we are to arrive at a ‘fair’ number) we can see that the difference between the high and the low FY 2020e multiple of 3.1 times is some degree greater than the 1.2 times difference between the high and the low earnings estimate for the same year:

Table 1: Apple Inc. Earnings and Valuation Estimates

| Number of Sell-side Estimates: 31 | FY 2020e Earnings | FY 2020e Multiple |

| High | $3.40 | 45.6x |

| Low | $2.76 | 15.0x |

| Mean | $3.22 | 35.0x |

| High Low Spread | 1.2 | 3.1 |

We can see this uncertainty at a market level by decomposing the market total return into the explanatory drivers of earnings growth, the change in the multiple paid for each unit of earnings and the dividend yield. As can be seen from the chart below, business performance (as captured by earnings growth) and investor sentiment do not always trend in the same direction:

Figure 1: S&P 500 Total Return Attribution

This means that in each discrete year, a correct call on the fundamentals can be undone by opposite sentiment in the market. To add further insult to injury, in some cases the fickle market can entirely reverse course the next year. For example, the 28 per cent multiple contraction experienced in 2018 was almost entirely reversed by a 25 per cent multiple expansion in 2019.

This suggests that holding stocks for short time periods increases the risk that one will experience a permanent loss of capital not from misreading the business, but from misreading the market.

Stocks for the Long Run

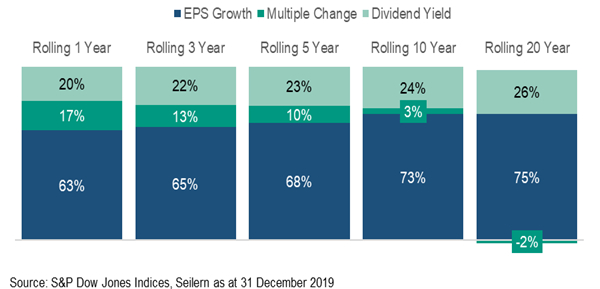

Once the holding period is lengthened, the picture changes. With each passing year, more weight is given to the business fundamentals and less to the whims of the market:

Figure 2: S&P 500 Total Return Attribution, Rolling Returns

The implication is important – the longer that you are invested in a security, the greater the likelihood that it is the business itself that drives the stock return, rather than a re-rating of that same stock driven by the market. Once holding periods extend into the ten-year and twenty-year range, returns are almost entirely explained by fundamentals. In the long term, fundamentals matter.

Only the Best Will Do

It isn’t enough to simply buy and hold any old stock for a long time period though. You must find and hold excellent businesses that have the characteristics that enable them to last for a long time. This has become increasingly difficult over time. A piece of research from Credit Suisse, an Investment Bank, illustrated the challenges of finding true long-term companies; with the average age of a company listed on the S&P 500 falling from almost 60 years in the 1950’s to less than 20 years today.

All of this comes back to a statement we made at the beginning of this piece: we look for businesses that can grow their earnings in a sustainable way. Investing in these businesses, Quality Growth businesses, achieves this purpose by allowing us to invest in excellent businesses that can sustainably grow over the long term, and by investing in companies that can be held over the long term, we increase the likelihood that this sustainable growth will in turn drive the share price.

1As opposed to the term ‘short-term investing’, which is an oxymoron.

2Here we are implicitly referring to the Price to Earnings ratio, the most commonly used metric to value a business.

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields