As uncomfortable as it is, we’re frequently reminded that markets are volatile, and where business results can be influenced by input costs that can triple in short order, we pay close attention. Yet, it is precisely in such testing environments that the true quality of a business is revealed.

Lindt & Sprüngli is not just another chocolate brand; it is a company that has spent nearly two centuries perfecting the alchemy of turning cocoa, a volatile agricultural commodity, into both a premium indulgence and a sustainable business. While Rodolphe Lindt’s 19th-century conching innovation established the benchmark for quality, the company’s true differentiation today extends beyond flavour. It rests on a vertically integrated, globally scalable business model that fuses industrial precision with the emotional allure of a luxury brand. Far from melting under the pressure of skyrocketing cocoa prices, Lindt has solidified its position, proving its competitive moat is deeper, and more durable, than many assumed.

The Bitter Reality of Cocoa and Lindt’s Resilience

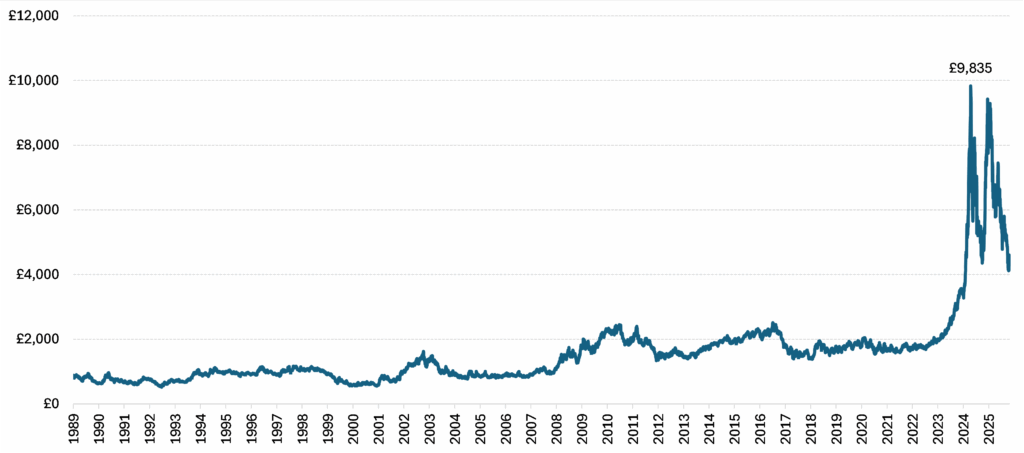

To appreciate Lindt’s performance, one has to first understand the extent of the recent headwinds. Over the past two years, cocoa bean prices surged, reaching an all-time high in April 2024, up over +390 per cent since the start of 2023 and over twice the record set almost 50 years ago (Figure 1).1

Figure 1: Historical Cocoa Prices, per metric tonne (GBP)

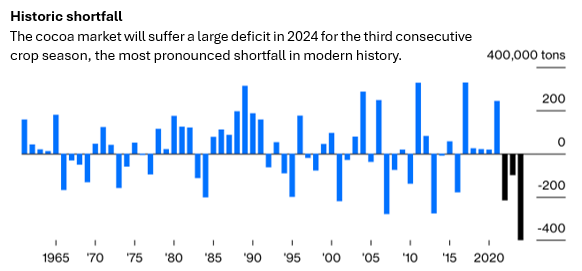

This surge was driven by a perfect storm of bad weather and disease outbreaks in West Africa, which accounts for approximately 70 per cent of global cocoa production. Specifically, the Côte d’Ivoire (36 per cent) and Ghana (10 per cent) account for nearly half of the world’s supply. The region is vulnerable to the El Niño phase of the El Niño-Southern Oscillation (ENSO) cycle, leading to intense heatwaves and drought. This weather volatility has also exacerbated disease outbreaks, with black pod disease spreading during extreme wet conditions in late 2023, followed by the spread of the swollen shoot virus during the subsequent dry spell. Other structural barriers, such as illegal gold mines2 and government-set cocoa prices that fail to benefit farmers from open market prices, also persist. This resulted in a large shortfall, marking the third consecutive crop season deficit in 2024 (see Figure 2). At the same time, non-structural factors such as market speculation drove some of this price action.

Figure 2: Global Cocoa Market Surpluses and Deficits

For Lindt, material costs account for one-third of sales, split roughly one-third cocoa, one-third other raw materials, and one-third packaging. Although there has been deflation in other raw materials and packaging, this has only partially offset higher cocoa and sugar costs.

Chocolate manufacturers like Lindt have therefore been faced with the difficult decision to either push pricing to protect margins and earnings (but at the risk that volumes may collapse), or to absorb these costs and sacrifice some earnings. Lindt has been able to adeptly navigate this, raising prices to fully cover inflation without destroying demand. Impressively, it has even gained share in markets such as the US.4 We attribute this to two key pillars of its competitive advantage: its vertically integrated business model and the pricing power its premium brands command.

Vertical Integration as a Strategic Advantage

Unlike many competitors who buy processed chocolate liquor, Lindt maintains a strict “bean to bar approach” – from sourcing premium cocoa beans from the world’s best regions of origin, to producing cocoa mass in its own production facilities, to moulding and packaging the finished product.5

In addition to guaranteeing quality, this also ensures its commitment to sustainability, with a focus on traceability and transparency. Through its Farming Program, Lindt ensures 100 per cent traceability of its cocoa beans.6 Amid cocoa supply shortages and decade-high inflation, controlling the production process from the bean up has also provided Lindt with a critical financial buffer versus peers who purchase cocoa mass from processors, such as Cargill and Olam, and/or outsource portions of the chocolate manufacturing process to producers like Barry Callebaut.

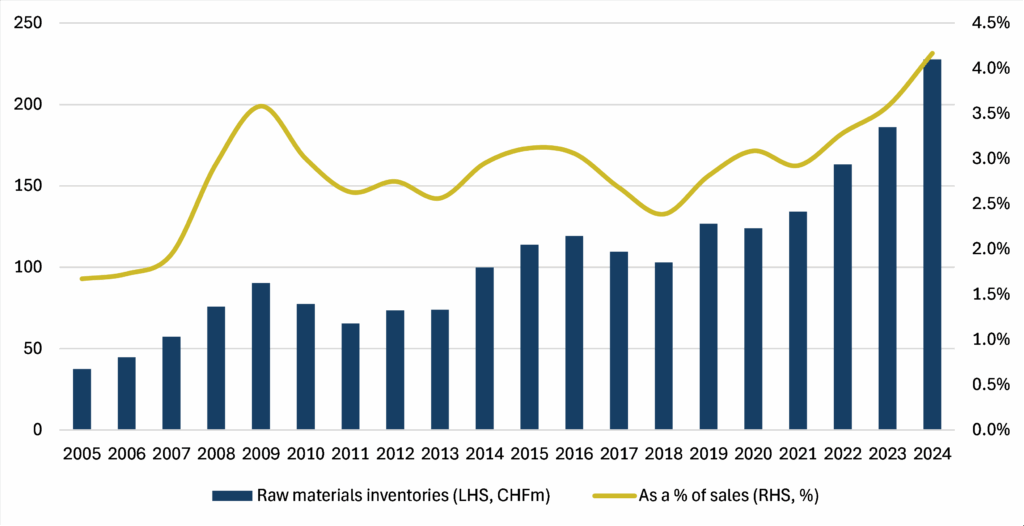

By securing long-term contracts and accumulating physical inventory in its warehouses, Lindt can draw down on lower-cost stockpiles (which have notably increased in recent years, see Figure 3). This delays the impact of spot market inflation on its income statement, preserving gross margins longer than peers who lack such buffers.7 Furthermore, in-house processing eliminates the markups charged by third-party intermediaries during periods of supply volatility.

Figure 3: Lindt’s Raw Material Inventories and as a Percentage of Sales

Pricing Power: The Shield of Quality

Lindt defines the premium chocolate market at a price point 50 per cent above the market average. While the global chocolate market is worth US$130 billion, the premium segment accounts for 20 per cent. Although Lindt only holds a 5 per cent share of the overall market, it is the leader in premium chocolate.8 With a goal of +6-8 per cent organic growth annually, the company targets an 8-10 per cent overall market share in the medium to long-term.

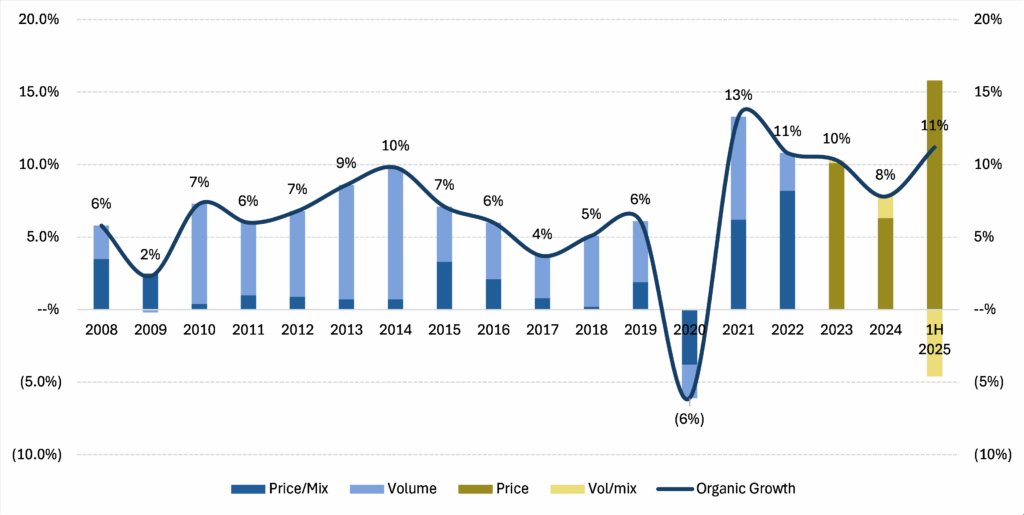

While the cost of cocoa tripled, Lindt has been able to grow just over +30 per cent organically (in aggregate) since 2023 thanks to implementing cumulative price increases of +35 per cent (+10 per cent in 2023, +6 per cent in 2024, and +16 per cent in 1H25, see Figure 4). In a commoditised industry, such price hikes would usually cause a sharp drop in volume as consumers switch to cheaper alternatives. However, Lindt’s volumes have remained stable, showing only minor elasticity in the first half of 2025 when they fell by just under 5 per cent, demonstrating its luxury credentials.

Figure 4: Lindt – Organic Sales Growth Decomposed

Companies who aren’t operating in the premium segment have been forced to take other measures. For example, some have experimented with shrinkflation; others have reduced the amount of chocolate they use in their products or replaced cocoa butter with cheaper equivalents such as palm oil. However, even these measures have not been enough to protect earnings. Mass-market peers like Mondelez (known for brands such as Cadbury, Milka and Toblerone) and Hershey are guiding for their full year 2025 adjusted earnings per share (EPS) to decline by approximately -15 per cent and -36 to -37 per cent respectively.9 By contrast, Lindt’s EPS is expected to grow by +8 per cent this year.10

Lindt’s resilience is due to the psychology of “affordable luxury”. While a +30 per cent price hike on a car or a house is prohibitive, a similar percentage increase on a premium chocolate bar, taking it from perhaps £3.00 to £4.00, remains within reach for most consumers. In difficult economic times, consumers may forego expensive holidays or dining out, but they will still treat themselves to a chocolate truffle. Lindt occupies this sweet spot: expensive enough to signal quality, but accessible enough to be a regular indulgence. In addition to this everyday consumption, around half of Lindt’s sales are focussed on seasonal occasions and gifting, with 20-25 per cent of sales coming in the Christmas period. Lindt’s luxury packaging and indulgent flavour makes it an affordable yet decadent gift at this time of year.

The Long View

While this episode of cocoa price inflation has demonstrated the resilience of Lindt’s business model, it also attests to the exceptional stability of its leadership. The company is run with a generational mindset, prioritising long-term brand equity over short-term noise. As Quality Growth investors, we seek companies that can grow their earnings sustainably, regardless of the economic cycle. Our investment in Lindt is not a bet on the price of cocoa beans, but an investment in a business that has proven it can turn a commodity with a volatile price into consistent, high-quality returns. Lindt’s steadfast pursuit of quality over quantity offers resilience against inflation and a high degree of predictability, reinforcing our conviction that it remains a great example of a Quality Growth company.

1This includes cocoa farmers selling their land to illegal miners, as well as miners encroaching on cocoa-growing areas, destroying farms and degrading soils and water resources, which is contributing to lower cocoa yields.

2In 1977 the cocoa price reached just over USD$5,000 per metric tonne.

3https://www.bloomberg.com/opinion/articles/2024-02-19/the-bittersweet-truth-behind-surging-chocolate-prices.

4Based on NielsonIQ data up to September 2025: Callum Elliott, CFA, ACA et al (Bernstein Societe Generale Group), Lindt (LISN.SW): Mea Cocoa, Upgrade to Market-Perform, Equity Research (26 September 2025).

5https://www.farming-program.com/en/bean-to-bar. The exception to this is Russell Stover and Ghirardelli which purchase chocolate mass.

6After achieving its goal to source 100 per cent of its cocoa beans through the Farming Program in 2020, Lindt extended the program to include cocoa butter in 2021 and cocoa powder in 2022. In 2024, Lindt sourced 84.2 per cent of its cocoa products, which includes beans, butter, powder, through the Farming Program or other responsible sourcing programs. It aims to achieve 100 per cent of all cocoa products by 2025.

7In addition to this strategy, Lindt also hedges with cocoa futures. In fact, the company took out longer-dated contracts as a result of its assessment of the evolving cocoa price situation.

8The top six global chocolate manufacturers in order of market share are: Mars, Mondelez, Ferrero, Hershey, Nestlé and Lindt.

9Mondelez, Q3 2025 Earnings Release, <https://ir.mondelezinternational.com/static-files/85657e60-8527-4f1f-b84c-ab5bdf236afe>; Hershey, Q3 2025 Earnings Release, <https://hershey.gcs-web.com/static-files/227fb818-6d03-4675-ae48-e5bd4cfe8014>. Although Mondelez and Hershey are not pure-play chocolate manufacturers it illustrates the cost pressures confectionary companies are facing. For example, for Mondelez, chocolate accounts for 31 per cent of FY24 revenues; Hershey does not disclose its revenues from chocolate confectionary.

10Mean Bloomberg consensus, as at 1 December 2025.

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields