Despite the dominance of dollar weakness in current headlines, a longer-term perspective presents a more measured story. For all the recent volatility, the relationship between the euro and the dollar has been remarkably stable when viewed over a multi-year horizon.

Consider the performance of the S&P 500 for euro-based investors versus US dollar-based investors. Over the past 10 years, the difference in cumulative returns is modest, 185 per cent for the euro-denominated index versus 201 per cent in USD, a mere 0.6 percentage points per annum. Stretch that horizon to 20 years, and the difference in compounded annual growth narrows even further, with euro returns slightly edging out those in dollars.

Table 1: Comparison of historic performance of S&P 500 in USD and EUR

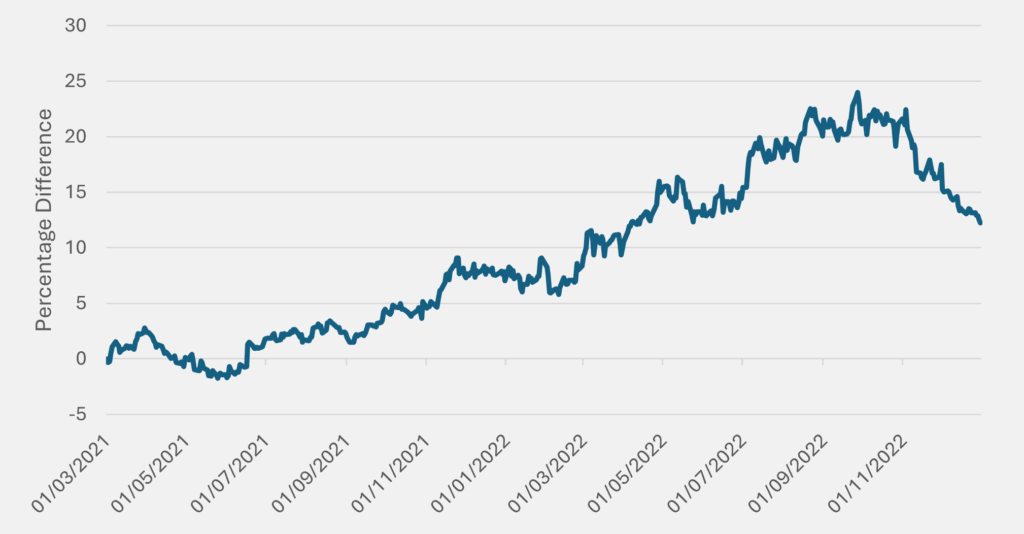

This consistency, however, offers little comfort to those contending with short-term currency swings. Between June 2021 and September 2022, for instance, the divergence between the USD and euro-denominated S&P 500 widened to 23 percentage points in favour of the euro-based investor. This is an extraordinary move over such a brief period. The disparity then partially reversed in the subsequent quarter, underscoring just how quickly sentiment and capital flows can shift.

Figure 1: Difference in Performance Between S&P500 USD and EUR Unhedged

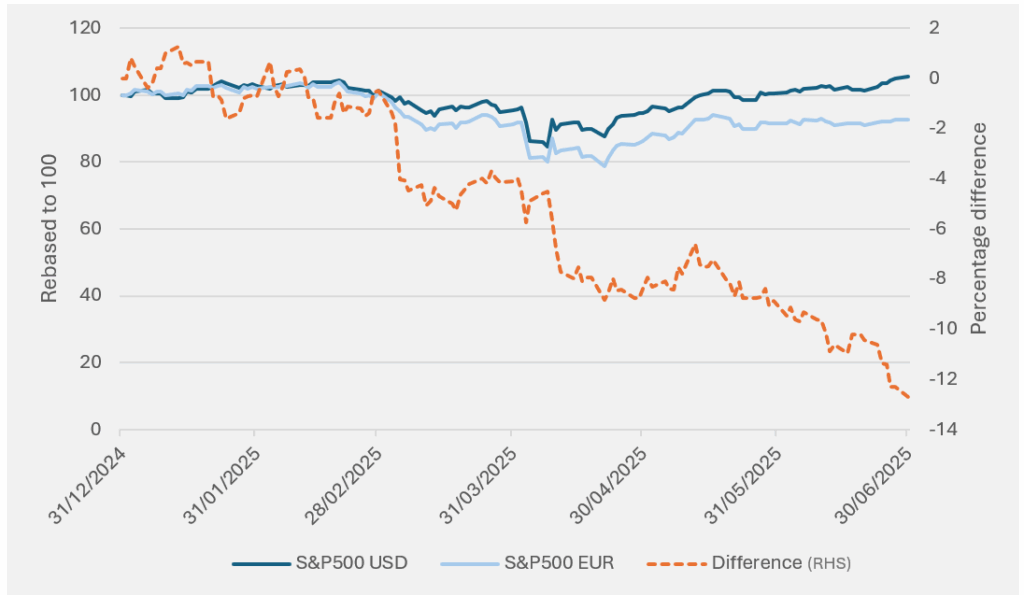

We find ourselves in a similar moment today, though this time to the detriment of the Euro based investor. Year-to-date, a US-based investor in the S&P 500 would be up around +5.5 per cent, while a euro-based investor—unhedged—would be down –7.2 per cent.1 This 13 per cent swing in just six months has been enough to prompt serious questions about the future role of the US dollar for international investors.

The Global Safe Haven currency

Given the degree of concern that currently surrounds the fate of the US dollar, one would be forgiven for forgetting that for most people’s careers the received wisdom regarded it as the ultimate safe haven currency. The dollar’s value may ebb and flow to reflect the health of the US economy, but whenever a real crisis reared its head investors would run for the safety of ‘King dollar’.

The historical precedent is compelling. In every major equity market sell-off of the past few decades, the US dollar has strengthened, and Treasury yields have fallen:

- During Covid, the S&P 500 fell -34 per cent, while the US dollar index (DXY)2 rose +3 per cent and the 10 Year Treasury Yield fell -78bps;

- During the Great Financial Crisis, the S&P 500 fell -57 per cent peak to trough, with the DXY rising +14 per cent and 10 Year Treasury Yields falling -182bps; and

- During the Dot-Com Bust the S&P 500 fell -49 per cent peak to trough, after many ups and downs the DXY rose +2 per cent and the 10 Year Treasury fell -262bps.

Those who bet against the US dollar in a crisis seem not to have considered the past. For a euro-thinking investor willing to take the currency risk, this was one relationship that did seem to provide some comfort over the years. In times of serious market distress, Treasuries and the US dollar would act as a safe haven, helping to cushion some of the blow from falling equity markets, at least in the very short term. Like most of life’s comforts, one quickly gets used to them and soon takes them for granted.

When the Anchor Drifts

Yet, on April 2nd this year, this relationship broke down in rather dramatic fashion. Not only did the past relationship not hold, it inverted. Between April 2nd and April 21st, the S&P 500 fell -9 per cent, with the VIX reaching levels last seen during Covid. This was a classic financial meltdown that traditionally would have led investors to seek refuge in the US dollar. Instead, the opposite happened. The US 10 Year yield rose +28bps in the same period and the DXY fell -5.3 per cent. These 13 trading days saw the USD, Treasury and equity prices all sell off strongly, bucking a trend which had held for a long time, and proving particularly painful for those Europeans investing in US assets who had not hedged their currency exposure. What is more, the US dollar has continued to weaken since then.

Figure 2: Performance of S&P500 USD & EUR Unhedged

Economists, trained in classical theory, were left scratching their heads. The imposition of tariffs, for instance, is supposed to strengthen a currency by reducing demand for foreign goods and hence foreign currency. Yet the dollar’s recent behaviour suggests investors are factoring in concerns far beyond trade dynamics.

Increasingly, it appears that political risk is being priced into US assets. From unpredictable leadership and murmurs of capital controls to proposals for punitive taxation and persistent fiscal deficits, the US no longer appears quite so invulnerable. The bear case for the dollar, once the domain of fringe commentary, is now echoed across mainstream headlines.

A Phoenix from the Ashes

At the same time, the narrative in Europe is shifting. For years, the continent was cast as the economic laggard, saddled with structural imbalances, stagnating growth, and fiscal rigidity. During the euro crisis, the dollar broke decisively higher against the euro, a move that held for over a decade. Brexit did little to help sentiment towards the UK, whose currency underwent a pronounced repricing.

Now the tide appears to be turning. Europe has embraced fiscal expansion, most notably with Germany loosening its purse strings, and defence spending has returned to the agenda with rare European unanimity. Infrastructure and rearmament have emerged as central policy themes, fuelling a rally in defence equities across the continent. This shift has been broadly based. European currencies have strengthened. Equity markets have moved higher. Bond yields have fallen, even as spending rises.

This resurgence, while nascent, is not going unnoticed. Asset allocators across the globe are recalibrating their views on the relative safety, and opportunity, offered by the US versus Europe. The dollar’s recent weakness, particularly against European currencies, is a reflection of those shifting capital flows.

On Companies and Earnings

These decisions ripple all the way down to our Universe companies and funds. When we look at the year-to-date US dollar performance of the companies in our investment Universe, we find that eight out of the top 10 are European companies.3 In many ways this should not be surprising. With large flows moving from the US to Europe we would expect European assets to rise. Furthermore, arguments about the under-valuation of European stocks versus US stocks have been the conversation topic of investors for years now, and a splurge of fiscal spending should surely lead to higher growth in Europe, which in turn should lead to upward earnings revisions for European companies.

Not what you might think: Valuation discrepancies, Cyclical Upswings and Tariffs

But, when we look at matters more closely, things may not be quite as clear. Within our Quality Growth Universe, for many years we have not observed a material valuation discrepancy between European and US holdings. In fact, on a discounted cash flow basis, our US companies are currently trading at more attractive valuations than their European peers.

Nor does the argument around upward earnings revisions necessarily hold for our portfolio. While it is true that Europe may benefit from fiscal stimulus and renewed growth, our companies, on both sides of the Atlantic, are generally less exposed to macroeconomic cycles since they do not rely as much on GDP growth to deliver earnings growth. This, after all, is a core tenet of Quality Growth investing.

Furthermore, concerns that tariffs will impair the earnings of our US companies are largely misplaced. As we discussed in our previous newsletter, the vast majority of our US holdings are not directly exposed to the tariff regime: they do not rely heavily on imported inputs nor are they particularly vulnerable to rising costs.

The benefits of a weaker US dollar

While our companies are less exposed to the headline risks that dominate market narratives, many actually stand to benefit from the weaker dollar. Our US companies derive over 40 per cent of their revenues from outside the United States. As the dollar weakens, those foreign revenues translate into higher US dollar earnings, creating a tailwind. While this does not offset currency depreciation entirely, it contributes a meaningful cushion via earnings upgrades.

In contrast, our European companies, which generate nearly 30 per cent of their revenues in the US, face the opposite challenge. Dollar revenues now convert into fewer euros, and their products become relatively more expensive to US buyers, especially if subject to tariffs. Together, these represent a modest but real headwind.

To be clear, these currency translation effects are incremental. They do not fully explain or negate the impact of broad currency moves. But in a world where small margins matter, they are not trivial either. And the greater the currency volatility, the more these effects will be felt.

Conclusion

We do not pretend to know how the broader geopolitical and macroeconomic landscape will evolve, but what we do know is that many of our US-based holdings, companies of high quality and global reach, are likely to see a tailwind from a weaker dollar. This currency effect, while not transformational, is meaningful. These incremental benefits will not undo the impact of large capital shifts or fully offset the magnitude of dollar weakness. But they will support earnings and may contribute to upward revisions in the quarters ahead. At present, little credit is being given to this dynamic.

The key point is that performance driven by fund flows or sentiment does not always align with fundamentals. In moments of narrative shift, whether about currencies, politics, or macro policy, it is tempting to draw sweeping conclusions. But Quality Growth investors must remain anchored to business fundamentals. Earnings power, competitive advantage, and resilience matter more than the temporary winds of capital.

1Year to Date Performance of S&P500 USD and Euro Unhedged; price return as at 30th June 2025.

2The Dollar Index measures the dollar against a basket of international currencies.

3From 31/12/2024 to 30/06/2025.

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields