A recent addition to the Seilern Universe, Autodesk exemplifies a software company that has embraced transformation not only frequently, but with genuine conviction. While nothing quite as dramatic as Bowie’s transformation into Ziggy Stardust has occurred, the company has repeatedly overhauled its business model over the past decade, often disrupting itself in the process. These transitions, however, have introduced volatility into Autodesk’s financial accounts, obscuring the underlying performance of the business, and at face value, threaten to breach one of Seilern’s Ten Golden Rules – Transparent Accounts. Yet, we believe from our research that these temporary distortions are the price of meaningful progress and come from a position of strength. The cumulative effect of these changes is a more transparent, predictable, and profitable business model, paving the way for the next phase in Autodesk’s evolution: the launch of its unified “Design and Make” cloud platform.

A Business Worth Owning

Founded in 1982, Autodesk has been a key player in the software industry for over 40 years. Its flagship product, AutoCAD, was the first mass-adopted computer-aided design (CAD) program, revolutionising 2D drafting for architects and engineers.

Since then, the company has primarily expanded its software portfolio into the Architecture, Engineering, Construction and Operations (AECO) and Manufacturing sectors. Digitisation, and consequently productivity, in these industries has historically lagged other sectors, held back by structural conservatism and inertia. This underpenetration presents a long runway for future growth, aligning well with our criteria for Superior Industry Growth and Strong Organic Growth.

In AECO, Autodesk’s most important market, its Sustainable Competitive Advantage is underpinned by its position as the only true platform player. This platform approach enables Autodesk to offer a suite of integrated solutions that span the entire building lifecycle, including post-construction operations. Early success with AutoCAD, combined with a series of strategic acquisitions, established Autodesk as the dominant force in design, the critical first phase of any construction project. From this position of strength, the company successfully expanded downstream into the pre-construction and construction phases, integrating its offerings across workflows. As a result, Autodesk has become a mission-critical partner to a broad range of industry stakeholders driving a highly sticky, recurring revenue model that is reinforced by significant barriers to entry for potential competitors.

Business Model Evolution

While underlying fundamentals are strong, Autodesk has undergone a series of business model evolutions that have introduced significant volatility into its reported financials, at times clouding our ability to assess the underlying performance of the business. On the surface, this may raise a red flag under our Transparent Accounts criterion, as opaque financial disclosure limits our ability to assess a company’s profit drivers and capital structure, and may indicate poor earnings quality. However, while these transitions have created temporary distortions, they have been strategically sound and proactively driven. Rather than reacting to competitive pressure, Autodesk has used its strong market position to reshape its model in ways that enhance financial predictability and drives cost efficiencies.

Perpetual Licensing to Subscriptions (2015–2016)

Autodesk was an early mover in shifting from perpetual license sales – such as one-off purchases of AutoCAD – to a subscription-based (SaaS) model, effectively leading its industries through this transformation. While the shift initially met with customer resistance, Autodesk encouraged adoption by offering multi-year subscriptions with upfront billing at a 5–10 per cent discount relative to annual contracts. Simultaneously, it applied pressure by increasing maintenance costs for perpetual licenses.

Leveraging its competitive strength and highly captive customer base, Autodesk began the transition in 2015 and completed it by August 2016, well ahead of many software peers, some of whom have still yet to fully adopt a subscription-only model.

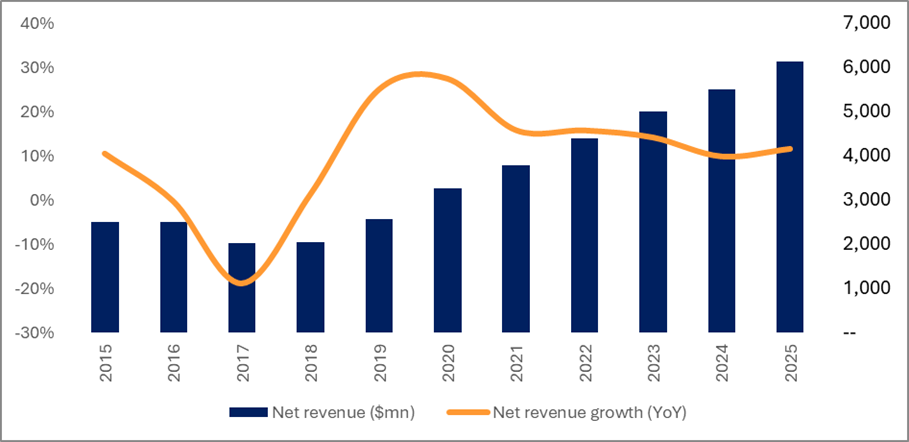

However, the financial impact extended well beyond that timeline. Between FY16 (year ending January 2016) and FY21, Autodesk’s reported revenue was significantly depressed due to the change in revenue recognition, shifting from large, upfront payments to revenue being recognised gradually over the life of each subscription – before more than recovering as subscription revenue accumulated. While this introduced substantial volatility, it ultimately gave way to higher-quality, more predictable recurring subscription revenue growth.

Chart 1: Autodesk Net Revenue by Fiscal Year

From Upfront to Annual Billing (2023–2024)

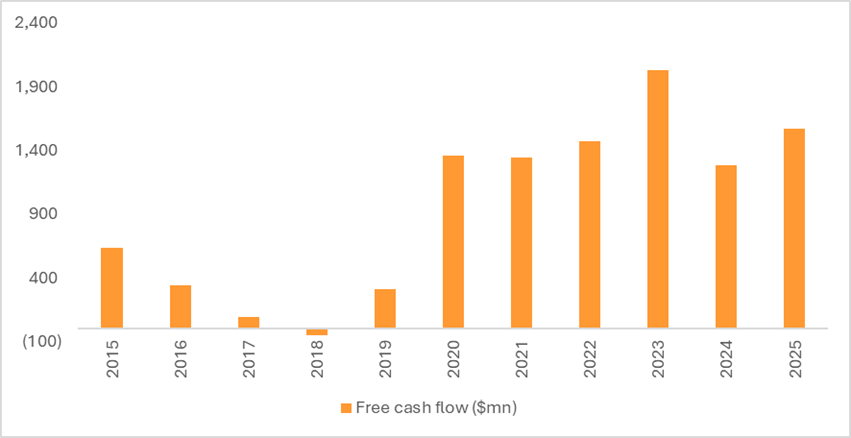

The next step for Autodesk was to strengthen pricing discipline by phasing out multi-year upfront customer billing, except for certain large enterprise agreements. While multi-year subscriptions remain available, they are now billed annually and no longer include discounts. This shift introduced short-term volatility to free cash flow, resulting in a sharp decline in FY24 and only a partial rebound in FY25. The disruption was largely due to a significant pull-forward of deferred revenue into FY23, as customers moved to lock in lower prices ahead of the billing change. Despite this near-term impact, the transition lays a stronger foundation for more predictable and higher-quality cash flow.

Chart 2: Autodesk Free Cash Flow by Fiscal Year

The New Transaction Model: Reclaiming the Customer Relationship (2024-2027e)

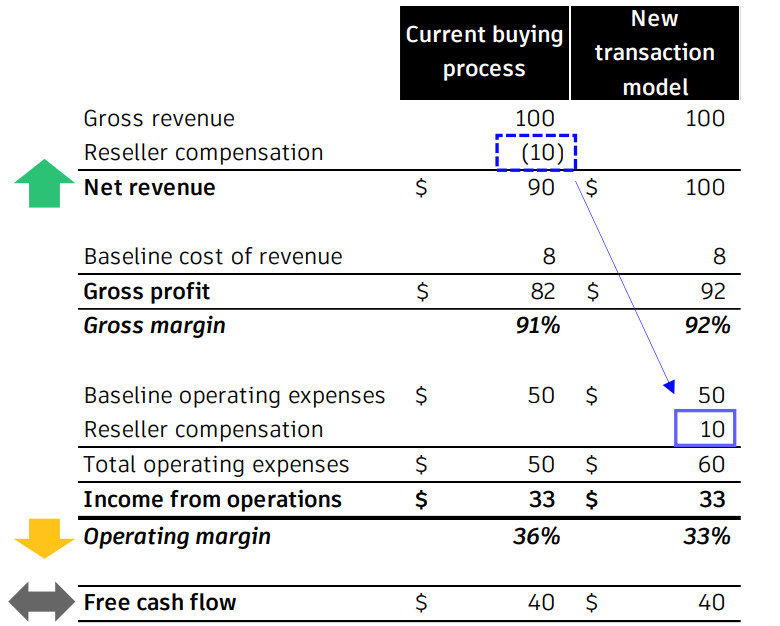

Moving to today and Autodesk is undergoing yet another change as it aims to transition its sales models to one where it transacts directly with customers. Currently, 58 per cent of Autodesk’s revenue flows through third-party channel partners who take a commission for each sale of Autodesk’s software. Under its new transaction model, the company is shifting sales to itself while encouraging resellers to pivot toward higher-margin, value-added services such as custom solutions. This shift, effectively forcing a change in reseller business models, has been made possible by the strength of Autodesk’s bargaining power, giving it the leverage to redefine its go-to-market approach. In doing so, Autodesk aims to unlock higher margins by reducing reseller compensation and expanding revenue opportunities through greater visibility into end-customer product usage, enabling more effective cross-sell and upsell efforts. Several companies within Seilern’s universe have successfully transitioned to direct sales models, which reinforces our confidence in Autodesk’s ability to execute a similar shift.

However, this transition is introducing more temporary noise into Autodesk’s P&L. Historically, reseller compensation was recorded as a contra revenue item, reducing net revenue. As transactions move direct, these costs are now reclassified as sales and marketing expenses. While this reclassification is neutral to dollar operating profit and free cash flow, it distorts optics:

- Net revenue growth is inflated, as reseller payments are no longer netted against it.

- Operating margin is suppressed, as those same payments now inflate operating expenses.

Figure 1: Illustrative Example of Autodesk’s New Transaction Model Accounting Changes

Not all reseller compensation will flow through operating expenses, as Autodesk expects to unlock cost efficiencies from direct transactions. While it is still too early to fully quantify the benefit, management has indicated expectations of multi-year margin growth stemming from the transition.

To aid investor understanding during this transitional period, Autodesk is publishing “underlying” revenue growth and operating profit figures that adjust for the impact of the new transaction model. However, audited financials are unlikely to provide a clean view of underlying performance until FY27 (beginning February 1, 2026), when the transition is expected to be largely complete.

While the latest accounting changes muddy the waters once more, the company’s history of similar adjustments, paired with transparent communication and sound rationale, gives us confidence that this reflects a genuine improvement in the business model, rather than an attempt to obscure something more concerning.

In the meantime, we anticipate Autodesk will offer further detail, particularly regarding the long-term margin benefits, at its upcoming Investor Day.

The Design and Make Platform: One Platform to Rule Them All

Autodesk’s next major evolution, the Design and Make Platform, marks a step change in how the company serves its customers, building on a decade of business transformation. Unlike previous shifts focused primarily on commercial models, this marks Autodesk’s most significant business model change to date, centred on a fundamental reimagining of its product offering. The company plans to consolidate its fragmented suite of over 100 tools into three integrated, cloud-native platforms tailored to distinct industries: Fusion for Manufacturing, Forma for Architecture, Engineering, Construction and Operations (AECO), and Flow for Media & Entertainment – though the latter remains a smaller part of the business. These platforms are designed to be cloud-native, meaning they are built and run entirely online rather than being installed on a user’s computer, allowing for real-time collaboration, automatic updates, and seamless access from anywhere.

At the core of these platforms is Autodesk Platform Services (APS), which makes it easier for users to share data and connect with external software. By bringing everything onto one system, Autodesk can introduce new technologies, like AI and digital simulations, more efficiently and deploy them across all its industry platforms.

Autodesk is rolling out its industry cloud gradually, one workflow at a time, and early benefits are already emerging. Gamuda, a leading infrastructure and civil engineering firm, faced significant inefficiencies due to fragmented data and manual processes during construction. By adopting Autodesk’s cloud-native tools to streamline permit management, Gamuda achieved a 91 per cent increase in productivity for handling digital permits, demonstrating the tangible impact of Autodesk’s platform-led approach.

Today, only around 10 per cent of Autodesk’s revenue comes from cloud-native products, underscoring how early the company is in this platform transition. But the long-term strategy is clear and rests on three pillars:

- Cloud Transition – Moving customers to cloud-based workflows and phasing out legacy desktop products.

- Unified Innovation Platform – Building new features, including automation and AI, once and deploying them across the platform to increase R&D efficiency.

- Ecosystem Expansion & Monetisation – Enabling external developers to build on the platform, improve interoperability, and ultimately generate new revenue through integrations and add-ons.

That said, these benefits will take time to materialise – most likely over the medium to long term. Customer adoption is tempered by performance concerns, design software is bandwidth- and computing-intensive, and by user inertia, with many preferring hybrid models over pure-cloud solutions. Additionally, Autodesk faces a prolonged period of “double spending” as it continues to support legacy on-premise products while investing in cloud-native development. These transitional inefficiencies look likely to persist for another five to 10 years.

Change for the Better

At Seilern, we are typically cautious of companies that frequently revise their strategies, as this can signal weak market positioning or a lack of competitive edge. Autodesk’s transitions have however been neither reactionary nor involved wholesale shifts in strategic direction. Instead, they have been deliberate evolutions of its business model, made possible by its strong competitive position. These changes, though reducing near-term transparency, have enhanced financial stability and price discipline, ultimately improving the transparency and predictability of the business.

Looking ahead, we believe the new transaction model – and ultimately, the rollout of the Design and Make Platform – will be meaningful profit drivers for the business. Beyond financial upside, the Design and Make platform strengthens Autodesk’s integration with its customers and reinforces its role as an indispensable partner at the heart of digital transformation across its industries.

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields