Starting a newsletter with a Warren Buffett quote is about as clichéd as it gets, but his description of the stock market behaving like a “psychotic drunk” feels particularly apt after the dramatic software sell-off so far this year. The pace and size of the decline at times looked less like a gradual debate about long-term growth and margins, and more like the sudden repricing that follows a profit warning or an accounting fraud. While it feels extreme, this is not the first time we have seen an increasingly impatient market shoot first and ask questions later. This newsletter looks at what has driven the capitulation, why the selling has been so indiscriminate across very different software businesses, and how we are assessing the balance of risk and opportunity.

From substacks to sell-offs

Although we have been living with ChatGPT and AI for more than three years, its impact on markets has, with a few isolated exceptions, largely been through the beneficiaries of the capex build-out. This began to change late last year as new model releases from OpenAI and Anthropic sparked a more direct fear that if AI could generate code, then software businesses were suddenly open to all sorts of new competition.

That fear accelerated with the launch of Anthropic’s Claude Cowork in January, which gave users access to autonomous agents capable of executing multi-step business workflows from natural-language prompts. This then intensified as Anthropic released a series of plug-ins for specific job functions from legal, to sales and finance. In so doing, they turned a conceptual threat into a visible disruptive tool. This led to hundreds of users posting on social media about the revolutionary productivity gains they were seeing, as magic began to unfold before their eyes.

It was remarkable how quickly markets assumed this breakthrough technology would soon disrupt the up-to-now most impregnable of tech business models. SAP, which only 12 months ago had been flying high at record valuations after almost tripling in value over the past two years, was all of a sudden deemed to be at huge risk of disruption. Its valuation fell by -33 per cent from September, back down to a price/earnings (P/E) ratio of 20x, a level to which Microsoft also sunk. And while Microsoft’s fall may also reflect fears of its elevated capex compressing future returns, it is notable that these two tech behemoths are now deemed to be worth less than many low growth, compounding Consumer Staple stocks like Colgate and P&G.

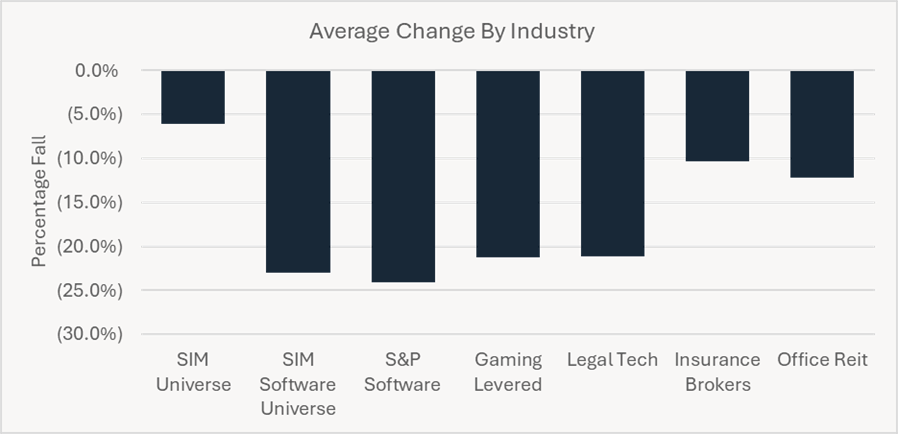

It was also remarkable how far and wide this disruption spread. Soon it was not only SaaS1 names caught up in this, but any industry with meaningful human judgement embedded in the value chain. Game developers, legal tech, insurance brokers, wealth managers, even commercial property and trucking companies were, at points, treated as if their business models were structurally impaired. This is where the already reflexive nature of markets met with the reach of social media echo-chambers, to combine into hysterical fear. A tech entrepreneur’s article2 on X, which painted a particularly apocalyptic picture, received 85m views, while a clip from an episode of ‘The Diary of a CEO’ podcast (50m downloads per month) showed a crypto investor citing that “knowledge was now worth zero”.3 In some cases this already seemed to be true.

Figure 1: Share price change of software affected industries during the software sell-off, January & February 2026

The panic arguably reached its fever pitch on 22nd February with the publication of the “Citrini Research” article, which painted another dystopian future, where improving AI capabilities would lead to widespread unemployment, mass protests and a large financial crisis. All of this by 2028. These articles and videos, helped by the increasingly large retail participation, had a major effect on stock markets. Incredibly, even a one paragraph comment contained in this sprawling piece of guesswork regarding the potential disruption of Mastercard and Visa, was enough to remove approximately $65bn from their combined market cap.

The fear of a conceptual threat

What seems to be going on here is that in trying to explain the scale of these moves, investors then leap to assume either that the disruption must be larger than previously thought, or that the probability of it happening must now be higher. Share price moves become the ‘evidence’ that then drives the narrative. We have of course been here many times before, which leads us to the famous quote of John Templeton on the four most dangerous words in markets: “This time is different”.4

Of course the issue with most bouts of market hysteria is that things are always a bit different, even if the behavioural biases and limitations of human psychology remain the same. This time does feel a bit different because this technology really feels like magic. Unlike, say, the fears around Mastercard and Visa being disrupted by Fintechs and cryptocurrencies, where the conceptual threat needed to be analysed at a distance through an arcane and unproven new technology, here everyone can use the tool directly. Even AI sceptics are stunned by the productivity improvements and granting of new powers across everyday workflows.

Furthermore, the speed of change is extraordinary. The early ChatGPT looks almost comical in comparison to the latest frontier models, such as Claude Opus 4.6, though we should not forget how mind blowing the original launch of ChatGPT felt at the time. Exponential leaps are being made in terms of capability. If these leaps continue, so the argument goes, maybe the scenario outlined in the Citrini piece is less implausible.

Yet, however tangible the immediate productivity gains now feel, whether they ultimately disrupt software and the wider “knowledge economy” remains a conceptual question. As things stand, most software companies’ earnings have barely moved. Some will be affected in the future, and some may be affected significantly, but others will not. Software spans a diverse set of businesses from relatively simple, modular tools like e-signature, to deeply embedded, highly complex “systems of record” that sit at the heart of regulated enterprise workflows. Despite this, we have seen a blanket sell-off and the indiscriminate nature of the selling is one aspect of this episode that is decidedly not new.

Capability vs reliability

So, what do we know? We know that AI is probably going to be transformative. We also have a high degree of confidence that the world isn’t going to be run by autonomous agents and robots in the short or medium term due to regulation, energy scarcity, slow adoption and, most importantly, the limitations of these models. If you listen to the leaders of the frontier labs, continued leaps in capability can sound inevitable. But there is also a clear reliability issue, rooted in how these models are built. A recent Princeton paper found that while benchmark accuracy is improving rapidly, reliability (defined as consistent behaviour, robustness, predictability and safety)5 lags behind. The difference here is between a car that looks fast on a racetrack and one that can be trusted on the motorway, in rain, or in roadworks: what it can do is not the same as what it will do, consistently, under real-world conditions.

It is important however, not to go too far and to dismiss the sell-off entirely. Some AI sceptics fall into this trap by arguing that the blanket sell-off implies these businesses are being priced to go to zero. Arguably the sell-off is, in many cases, merely a reflection of higher uncertainty around margins, competition and durability of growth. Therefore, a higher discount is being applied to a group of companies which were already carrying elevated valuations. These are valid concerns. Even so, we know that not all software is created equal and some will remain more protected and therefore deserve a higher valuation.

How does one tell which companies are going to survive with their current strengths in place? Many different frameworks are doing the rounds from the sell side, on social media and, of course, in substacks. These often focus on probabilistic versus deterministic software, the presence of proprietary data, and whether revenues are tied to seat-based pricing. While this is at least a more nuanced approach than “sell everything that touches software”, in many cases these initial attempts are also too blunt.

Take the seat-based pricing risk. The logic here is clear: if an agent can do the work of multiple humans, fewer seats are required, and seat-priced revenue will fall. But the real question is not whether a company charges per seat; it is how adaptable the commercial model is, and how essential the tool is to the customer. If the product is genuinely differentiated (even in a world of agents) and the vendor can shift towards consumption pricing or enterprise agreements, then seat-based pricing becomes a commercial transition rather than an existential flaw. The real vulnerability is therefore not just whether a company charges per user, but a combination of weak differentiation, slow adaptability, and cheaper competition arriving first.

There are, in practice, multiple AI-related risks for software companies and they will affect different businesses, to different degrees, in different ways. Crucially, they must be weighed against each company’s defences to those risks, and against the opportunities AI creates. In some cases, AI disruption is going to lead to lower growth and lower margins. But in others, we think the risks have been overstated and therefore the low valuations represent very attractive buying opportunities. AI may also create opportunities by strengthening the business model of the incumbents, an argument receiving little airtime right now. All these things can be true at the same time; the key is working out which one is which.

Conclusion

So far, we see little evidence of material AI-driven disruption across the companies in our universe, and we have identified only a small number where that could plausibly change in the near term. We remain vigilant, mindful that we may be witnessing the biggest technological revolution since the internet. We are also aware of the complexity and complications of the real world. A highly capable, but erratic and unreliable agent may be acceptable if you are a start-up pushing out marketing emails or launching a new app with no users. But large businesses, operating in mission-critical and highly regulated industries are governed by controls, auditability and accountability and require near perfect consistency and reliable execution. That is why we expect adoption to be uneven and, in many areas, slower than the most breathless of recent narratives imply. Our response is to remain focussed on empirical evidence. We will test where AI is genuinely changing customer behaviour and economics, distinguish between businesses with durable defences and those without, and act with discipline rather than speed.

1Software-as-a-Service (SaaS) is the name given to software delivered over the internet, hosted and continually updated by the vendor, rather than installed and maintained on a customer’s own systems. The model emerged in the late 1990s and was popularised by early pioneers such as Salesforce. Today, “SaaS” is used as shorthand for subscription software more broadly.

2“Something big is happening”, Matt Shumer, X, 10th February 2026.

3“The Diary of a CEO” interview with crypto investor Raoul Pal, was originally published in November 2024.

4The correct quotation of Sir John Templeton is “The investor who says, “This time is different,” when in fact it’s virtually a repeat of an earlier situation, has uttered among the four most costly words in the annals of investing.” 16 Rules for Investment Success by Sir John Templeton.

5“Towards a Science of AI Agent Reliability”, Rabanser, Kapoor et al., Princeton University, 24th February 2026.

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields