In his well-known 1994 book, Increasing Returns and Path Dependence in the Economy, Professor Brian Arthur put forward an argument which, at the time, created quite a ripple within both the academic and investment circles. The crux of his argument was that the law of diminishing returns1, which had been well entrenched for over a century amongst the economic cognoscenti, would no longer hold true for the future, knowledge-based economy. Indeed, this new section of the economy would actually be driven by increasing returns. As it was put:

“Increasing returns are the tendency for that which is ahead to get further ahead, for that which loses advantage to lose further advantage. They are mechanisms of positive feedback that operate—within markets, businesses, and industries—to reinforce that which gains success or aggravate that which suffers loss. Increasing returns generate not equilibrium but instability: If a product or a company or a technology—one of many competing in a market—gets ahead by chance or clever strategy, increasing returns can magnify this advantage, and the product or company or technology can go on to lock in the market.”

Fast forward almost thirty years, and investors might say that Professor Arthur was not far off the mark. Indeed, there appear to be large sections of today’s economy which have been able to demonstrate an incredible durability of growth, well beyond what economic textbooks would suggest is theoretically possible. To be clear, the law of diminishing returns is still alive and well, however, it predominately rules over the traditional parts of the economy, namely the bulk processing of resources.

The principle of increasing returns should not come as a surprise to the quality growth investor, although these types of companies are indeed atypical. A dominant feature of a quality growth company is its ability to generate a strong and stable level of growth, which can then be sustained for long periods of time. In many instances, this can be over multiple decades.

A quality growth company can achieve this through a number of ways including establishing powerful network effects; providing mission-critical non-core products or services to its customer (Searching for the (non) core); achieving scale through structural cost advantages; or building a wide moat from the quality and reputation of its brand.

So, how do we think of increasing returns in the context of the Seilern Universe? Here, there are a few things to unpack.

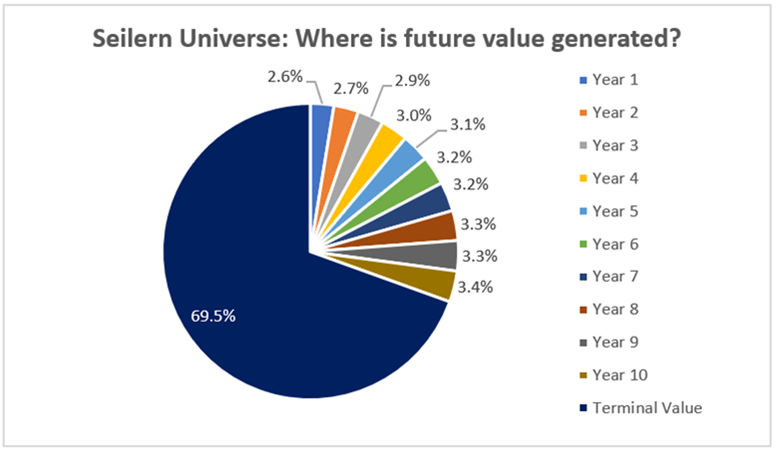

The first is that if you’ve invested in a company which has defensive and durable growth, then the bulk of that company’s value comes from the cashflows it is able to generate after year five (The price isn’t always right). Indeed, for the average Seilern Universe company, around 86 per cent of its total value comes from these longer dated cashflows.

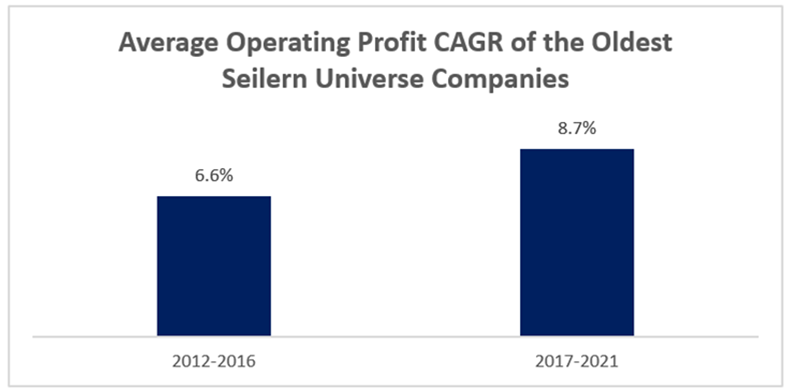

Secondly, investors often underestimate the longevity of profit growth that can be generated for quality growth companies. Success of this can only be seen over time. The below chart includes only companies which have been held in the Seilern Universe for longer than ten years (there are thirty companies in total). To demonstrate this longevity, we’ve calculated an average compound growth rate for this group of thirty companies, split between two time periods: the first five years (2012-2016) and the next five years (2017-2021). Despite the inclusion of COVID-19 in the latter period, the average Seilern Universe company within this elite group was able to record a healthy 8.7 per cent CAGR from 2017-2021. More importantly, this rate of growth demonstrates increasing returns given that it is over 30 per cent higher than the first period.

Thirdly, investors who have the luxury of time to thoroughly research companies, drastically increase their odds of forecasting with any degree of accuracy. To expand on the above example with a question: what do you think the likelihood would have been, back in 2011, that the market was forecasting that the future cashflows of these thirty companies would exhibit increasing returns? I would imagine very few if any at all. This point is crucial because it goes to the heart of understanding a company’s true value.

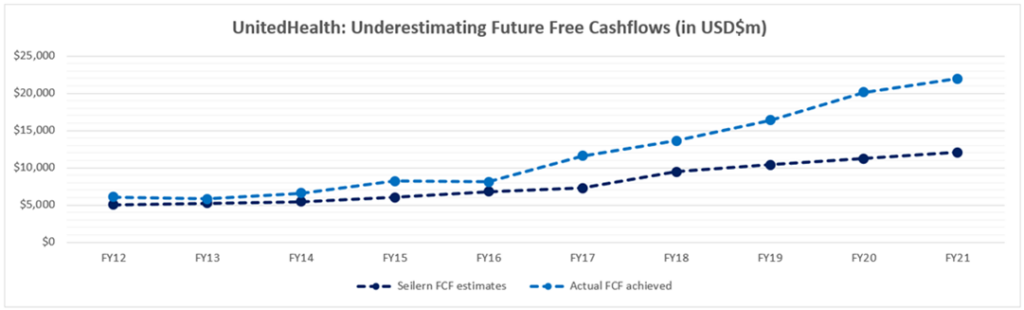

A real-life example should help to drive this message home. Below we’ve put together two sets of data for a company which has been in the Seilern Universe for over fifteen years – UnitedHealth Group. The dark blue line represents the free cashflow forecasts we made each year for the company, which, at the time, looked forward at least five years into the future. The light blue line represents the free cashflows that UnitedHealth has subsequently been able to generate over the last decade.

You can clearly see that for the first five years (2012-2016), the two lines aren’t materially different. This is not at all uncommon when valuing a company: an investor’s near-term forecasting tends to be more accurate. The real divergence, however, starts to happen from year six onwards (2017-2021). Indeed, a long time ago we had forecast that UnitedHealth would generate $50 billion in free cash flows during this latter period, whereas the company was actually able to achieve $84 billion. Over the entire 10 year period, we underestimated the company’s free cashflow generation by close to 50 per cent. As you can imagine, this would have led to a sizeable underestimation of the company’s true value at the time.

It’s for this reason that we tell clients that our forecasts will be incorrect over the long term, but that they’ll likely be incorrect in terms of undershooting the actual upside. In essence, trying to value a quality growth company with high and durable recurring revenues helps us reduce the risk of making a forecasting error on the downside.

Bringing this all together, many industries around the world are experiencing rapid scalability and a ‘winner takes most’ market. The knowledge-based economy has given rise to many companies that have been able to lock-in large parts of the market. This has not only allowed them to keep growing, but has also allowed them to achieve an accelerated rate of growth. This increasing returns environment is somewhat in contrast to the well-established school of thought that all companies will suffer from diminishing returns over time and, therefore, mean revert. Unfortunately, the reality is that diminishing return assumptions tend to be the default valuation framework across much of the financial market community.

Given our belief that the value of a company is generated from its long term cashflows, we look at apparently expensively valued companies differently to many others. We do not take the classic short cut and conclude that the company is now overvalued because its share price has performed well, and that it should therefore mean revert. Instead, we focus our attention on our qualitative research, which helps us assess the likelihood that a company will be able to grow into its valuation over time. More often than not with our companies, we conclude that they are well deserving of this higher valuation.

1The assumption of diminishing returns: products or companies that get ahead in a market eventually run into limitations, so that a predictable equilibrium of prices and market shares is reached.

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields