An old saying among US stock market aficionados claims that the trading days following the Labour Day holiday will be indicative of the mood of markets in the weeks and months leading up to year-end. Were that to hold true this year, the weeks ahead will prove to be complicated as confidence is currently in short supply. This was clearly evident in the month under review.

It is generally accepted that the inflationary pressures that bedevilled the past two years are abating and that inflation numbers, as well as expectations in the future, have substantially retreated from their highs this and last year. Even pronounced hawks across markets, media and central banks have adjusted their message. However, this message was recently universally re-conveyed across most leading western central banks (if not all) and was not warmly received by financial markets across the world. In essence, the new buzzwords causing anxiety across bond markets and, by extension, stock markets are “higher for longer” and “getting the job done”. Through these messages, which were received loud and clear, central bankers are warning that, despite improved inflation numbers, the day on which interest rates will begin a new downward trajectory is firmly not yet on the horizon.

The first and most important question surrounds the differential in bond market yields across their various maturities, that is the yield curve. When markets expect a combination of economic stagnation and persistent inflation, short-term interest rates produce a higher yield (in anticipation of continued inflation) than long ones (in anticipation of economic stagnation or downturn). This was the primary cause of the inversion of the US 2y-10y yield curve (commonly known as the 2s10s curve), which has been in this state for well over a year, the longest inversion since 1981. Currently, however, statistics have surprised observers in showing a dogged determination of the world’s leading economy, the US, to continue to grow in spite of a relaxation of the previous labour market rigidities (albeit a mild relaxation). This would indicate that the background to a persistent inverted yield curve is old-fashioned and no longer applies to the current state of affairs.

Other leading economic blocs, such as China and the European Union, have produced no pleasant surprises, on the contrary. As China grapples with ongoing pressure on the Renminbi and the Chinese central bank continues to manage the external value of its non-floating currency (also subjected to capital controls) through minute intervention, the EU and its leading economy, Germany, is confronted with an economic stagnation at best. Germany is now regularly described as the “sick man of Europe”, to the delight of the UK.

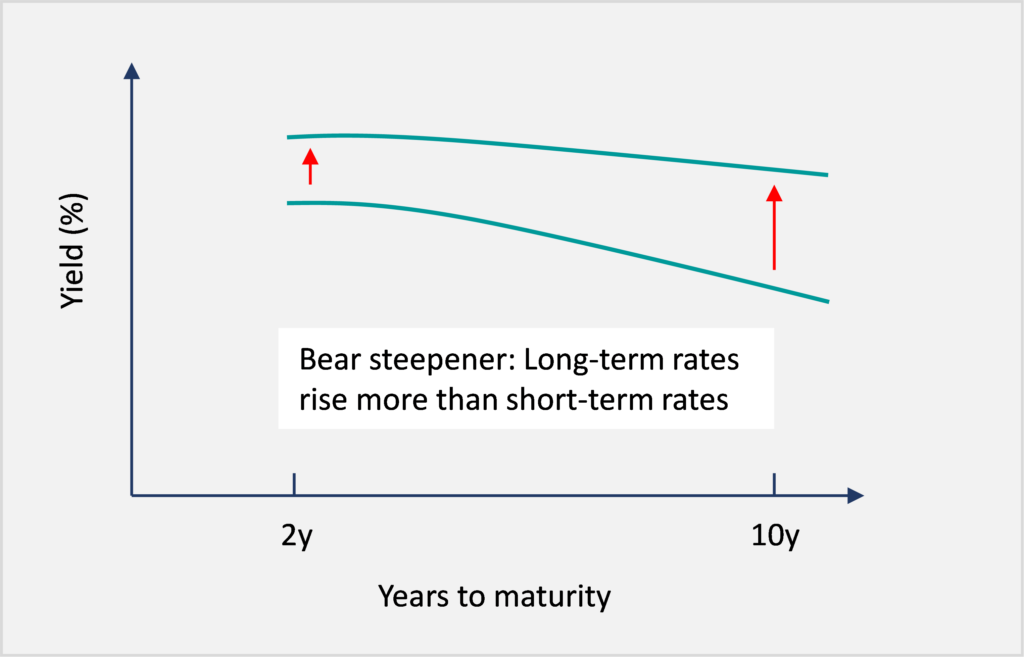

A closer look at what has occurred in the shape of the US bond yield curve is warranted at this juncture. Starting in early July, the spread between long and short yields has fallen from the extreme levels earlier in the year. Although this is nominally good news, the end result may be a narrower spread between higher interest rates across all maturities. This so-called bear steepener movement has come (at least in part) from the combination of increased US treasury issuance coupled with a realistic expectation that artificial intelligence will give a renewed push to US economic growth. This has caused long bond yields to explode. Were this to last it would not augur well for overall confidence, indeed it has already caused anxiety among investors. Nor would it help US corporate margins, as companies have extended their debt duration in the last few years. All this has happened as the inflation problems take a back seat, even as oil prices have pushed higher.

Figure 1: Example of a bear steepening yield curve, both curves remaining inverted

Less often discussed, however, is that today’s bond vigilantes have positioned themselves accordingly. A glance at hedge funds’ short positions at the long maturity end of the bond market probably reveals that sooner or later short-covering will take place, thus making a reversal of rising yields, or a short squeeze, a sure thing. For the moment, however, this scenario has not yet been seen.

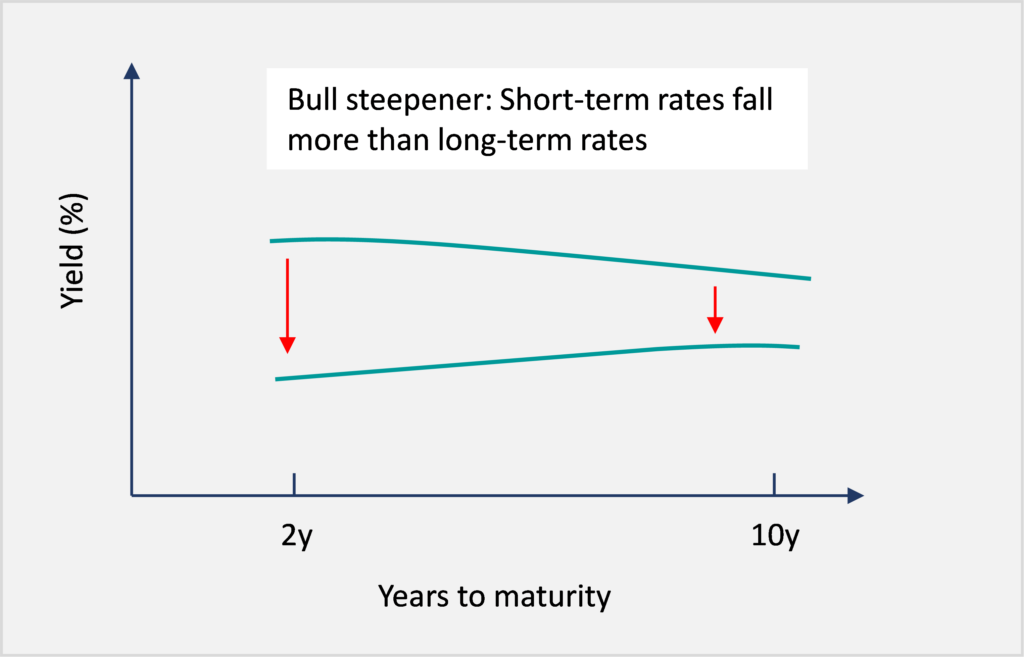

What about the bull steepener?

Under this background, the sharp rise in bond yields will have heightened the risk of future economic weakness and how it plays into the labour market. The inevitable result will be fewer jobs created, less tension in labour markets leading to a fall in bond yields across all maturities. Here, shorter-dated ones will fall sharper and faster than longer maturities. In the end, the yield curve will have reverted to normality.

Figure 2: Example of a bull steepening yield curve, ending with a disinverted (normal) yield curve

It is not intended to predict which of the two steepener scenarios will play out. But, either way, multinational Quality Growth businesses will not suffer a margin erosion to their businesses (all other things being equal), at least not from the development of the yield steepener and the disinversion. Whilst share price volatility may well affect such companies, volatility of underlying profits is well removed from the vagaries of the bond markets.

And that is what counts.

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields