The further into the future profits will continue to grow, the higher the price-earnings ratio an investor can afford to pay.

If the job has been correctly done when a common stock is purchased, the time to sell it is – almost never.

There are a relatively small number of truly outstanding companies. Their shares frequently can’t be bought at attractive prices. Therefore, when favourable prices exist, full advantage should be taken of the situation.

Philip Fisher, Common Stocks and Uncommon Profits

One of our common sayings at Seilern is that “you cannot value that which you don’t understand”. In other words, if one has not conducted detailed analysis on a stock and has not obtained an intimate level of knowledge regarding the durability of its future earnings, there is little point in attempting to value it. This is why we do not discuss valuation when we are researching prospective investment ideas to add to the Seilern Universe. If we were to do this, we would run the risk of being misguided by something we could not yet verify. Once a stock has been unanimously approved into the Universe, it becomes the responsibility of the portfolio managers (or ‘risk managers’ as we like to call them) to build a well-diversified and concentrated portfolio of stocks, at reasonable prices.

Let us explore what ‘reasonable’ in this context means.

Across Seilern’s Universe of approved companies, there are on average 25 sell-side brokers who cover these stocks. Given the enormous amount of resources and capital dedicated to this sell-side space, one would naturally ask how we could possibly add any value? The answer to this is rather nuanced. From this average, 23 sell-side analysts forecast earnings out one year, 16 forecast out three years, and only 2 bother to forecast out to five years. This is akin to saying that a company will have zero growth in five years’ time. How many investors realistically think that of the likes of Mastercard or Google? This sharp drop-off in sell-side coverage is very important for us, as it demonstrates the short-term thinking that a large portion of the investment community adopts.

Long-term investors are thus well-positioned to take advantage of this short-termism. Having an intimate knowledge of our companies gives us high levels of conviction regarding the sustainability of their earnings, which is often much further out than five years. This is where we believe we add value. Whilst our exact earnings forecast for a company in ten years’ time will inevitably be wrong, if it is ‘roughly right’ and we believe that the value of a stock is a function of its future cash flows discounted at an appropriate rate, then building ten-year discounted free cash flow models should reveal a stock’s true long-term upside. We are able to do this because we invest in companies with strong pricing power and high levels of recurring revenues, which improves our longer-term forecastability. When this upside will be realised is anybody’s guess, however, our view is that investors can drastically increase their odds of realising this value by holding the company for a long time. In theory, this period extends into perpetuity. Therefore, valuation derived from a discounted cash flow model is a superior indicator of ‘reasonable’ compared to relative valuation techniques such as price-to-earnings.

I would like to explain ‘reasonable’ in another context, which should also address the misconception investors often have regarding the purchasing of stocks with ‘optically’ high price-to-earnings multiples. Fundamentally, we believe that over the long-term, a company’s share price will grow broadly in-line with its earnings growth. Keeping the level of earnings growth constant, if along the way there are periods where its share price grows faster than its earnings, a stock will see its multiple expand (thus becoming more ‘expensive’ in common parlance). If its share price lags its earnings growth, then its multiple will compress (becoming ‘cheaper’). Investors often consider this compression to be a signal of danger. In reality though, there are three common reasons why a multiple might compress; 1) a company grows into its valuation over time, 2) investor confidence in the stock wanes, leading to a fall in its share price whilst its expected earnings growth remains broadly unchanged; or 3) a company’s earnings start to decelerate (or even fall) more than the market had anticipated, and investors accelerate this downward momentum by selling its shares at a faster rate. It could be argued that only the last of these three scenarios poses a real sign of danger. The key decision we therefore need to make is to ensure we are investing in companies that are able to sustain a decent level of earnings growth, which then underpin a ‘reasonable’ valuation. For Seilern, this earnings growth has historically been in the 10 to 15 per cent range.

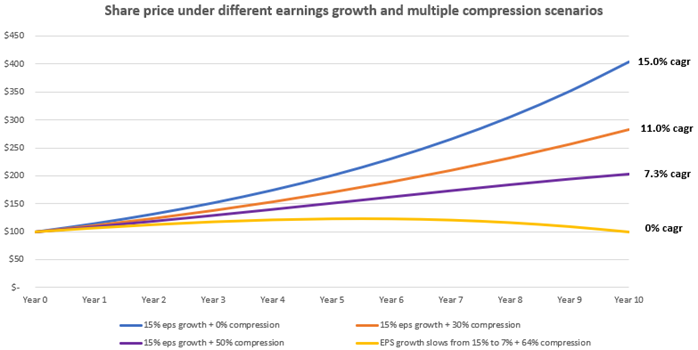

Let’s take a hypothetical stock which is trading at a forward price-to-earnings multiple of 40, which many in the community of conventional wisdom would consider to be an ‘expensive’ stock. Below I’ve charted such a company’s share price projection over a ten-year period based on a number of earnings growth and multiple compression scenarios.

This chart mathematically demonstrates that if a company on a multiple of 40 can grow its earnings annually by 15 per cent, it should achieve a 15 per cent compounded annual return over ten years (assuming no dividends and a stable multiple). If this same company experienced a 30 per cent decline in its multiple over the investment period (from 40 to 28), because its earnings growth remains strong, it should still deliver a compounded annual return of 11 per cent despite the compression headwind. For this investment to achieve a compound annual return in line with the long-term equity market average of around 7 per cent, this multiple compression would have to be 50 per cent (from 40 to 20). Most telling, perhaps, is the last scenario. Even if earnings growth slowed sharply from 15 to 7 per cent over this ten-year period, the investment would still be breaking even with a 64 per cent multiple compression (from 40 to 15). Under all scenarios, the company has essentially ‘grown’ into its valuation, which has provided downside protection given it has been underpinned by sustainable earnings growth.

A real-life example of this concept is our long-term investment in Alphabet. Since its peak price-to-earnings multiple in late 2007 of 44, the company has seen its multiple compress by 55 per cent to 20. Whilst this could be perceived to be a headwind for the company’s valuation, it is in fact not the case. During this 16-year period, Alphabet has managed to grow its earnings by a compound annual rate of 19 per cent, which has in turn driven a 13.5 per cent annual compound return in its share price (663 per cent cumulatively compared to 197 per cent for the S&P 500). Unfortunately, those investors who had valued Alphabet on an overly simplistic price-to-earnings multiple back in 2007, and feared a possible multiple compression, would not have enjoyed the stellar returns which took place despite what happened during the global financial crisis.

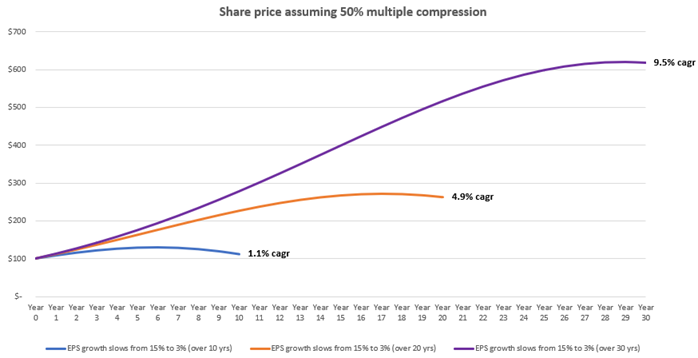

Another theoretical example worth sharing takes an even longer-term view. Below is a chart showing three different scenarios for the same stock we used in the previous example. It assumes a sharp 50 per cent multiple compression (from 40 to 20), however this happens over different periods of time (ten, twenty and thirty years). It also conservatively assumes that earnings growth will gradually slow to a long-term 3 per cent global GDP rate under all three scenarios. What it clearly demonstrates is that the longer the holding period and the longer the ‘fade’ rate of its earnings growth, the less a stock will be impacted by multiple compression. This is illustrated by the fact that, despite a 50 per cent multiple compression and a slowing earnings profile from 15 to 3 per cent over a 30-year period, an investor would still achieve an attractive 9.5 per cent compound annual share price growth (assuming a disciplined buy-and-hold strategy).

In conclusion, the key to the above examples is finding companies which we think can compound an acceptable level of earnings growth over many years, and our Ten Golden Rules provide a rigorous framework for assessing this durability. Other than buying stocks when opportunities arise from acute falls in the market, there’s usually no ‘right’ time to buy quality growth companies for investors with very long-term horizons. As the arguable grandfather of growth investing, many of Philip Fisher’s investment ideologies strike a chord with our own investment philosophies. Perhaps none more so than the belief that after having conducted thorough analysis on a company, adopting a buy-and-hold strategy and being disciplined in times of fear, should lead to superior risk-adjusted returns over the long-term.

This is a marketing communication / financial promotion that is intended for information purposes only. Any forecasts, opinions, goals, strategies, outlooks and or estimates and expectations or other non-historical commentary contained herein or expressed in this document are based on current forecasts, opinions and or estimates and expectations only, and are considered “forward looking statements”. Forward-looking statements are subject to risks and uncertainties that may cause actual future results to be different from expectations.

Nothing contained herein is a recommendation or an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment advice. The content and any data services and information available from public sources used in the creation of this communication are believed to be reliable but no assurances or warranties are given. No responsibility or liability shall be accepted for amending, correcting, or updating any information contained herein.

Please be aware that past performance should not be seen as an indication of future performance. The value of any investments and or financial instruments included in this website and the income derived from them may fluctuate and investors may not receive back the amount originally invested. In addition, currency movements may also cause the value of investments to rise or fall.

This content is not intended for use by U.S. Persons. It may be used by branches or agencies of banks or insurance companies organised and/or regulated under U.S. federal or state law, acting on behalf of or distributing to non-U.S. Persons. This material must not be further distributed to clients of such branches or agencies or to the general public.

Get the latest insights & events direct to your inbox

"*" indicates required fields